RWA Tokenization Nears $30B but DeFi Use Stays Low

Tokenized real-world assets have grown to nearly $30 billion on-chain, yet fewer than 10% are actively deployed in DeFi protocols. This structural gap between RWA tokenization and composability remains a key challenge for institutional adoption.

Yuri Konnov

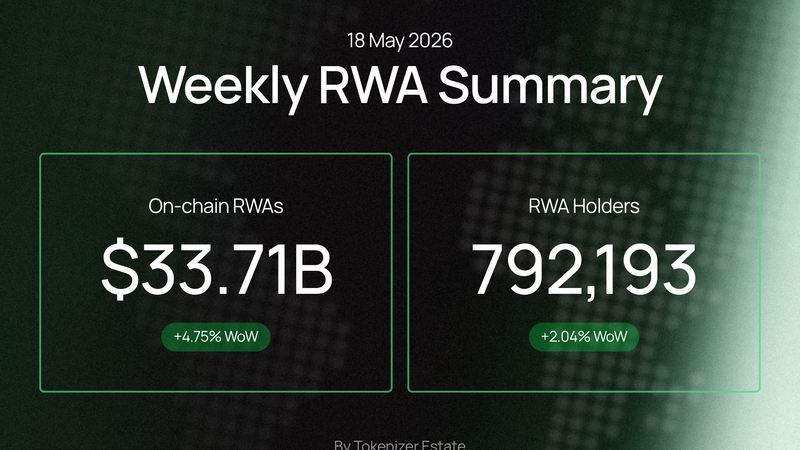

Tokenized real-world assets stabilized at $30 billion in on-chain market capitalization in mid-May 2026, yet CryptoSlate's composability gap analysis published May 18 found that fewer than 10% of that total is actively deployed in permissionless DeFi protocols — a structural divide that separates institutional ownership rails from the programmable finance infrastructure that originally motivated on-chain asset issuance.

The concentration of value in compliance-constrained products is stark. Tokenized U.S. Treasuries climbed to $15.20 billion, and government debt now accounts for more than 60% of the tokenized RWA market when measured by protocol assets under management. Products from BlackRock and Circle led inflows into that category, and both are built on permissioned transfer frameworks — allowlisting, KYC gating, and transfer-agent reconciliation — that structurally prevent direct integration into open protocols such as Aave or Uniswap. The result is a large pool of on-chain assets that cannot be pledged, borrowed against, or composed without operator intervention.

Individual product figures illustrate the bifurcation. Ondo Finance's tokenized Treasury products held near $2.7 billion in total value locked, while Circle's USYC crossed $2.9 billion. Both sit within the Treasury segment that dominates headline RWA figures, yet their DeFi-active portions remain a fraction of notional value. The total number of asset holders across the RWA market reached approximately 759,700, a 4.76% increase month-over-month, indicating that wallet-level adoption is widening even as DeFi deployment ratios stay low. Monthly transaction volume, however, fell 25.68% — the largest single-month drop recorded in recent periods — suggesting that holder growth and active protocol usage are diverging.

The regulatory framing around this gap has grown more explicit. On April 2, 2026, the International Monetary Fund published a note titled "Tokenized Finance". Tobias Adrian, the IMF's Financial Counselor and Director of the Monetary and Capital Markets Department, argued that tokenization is not a marginal efficiency improvement to existing financial infrastructure — a position that implicitly challenges the current model in which most tokenized assets replicate traditional custody and transfer constraints on-chain rather than enabling new settlement or collateral mechanics. The IMF note, reported by FinTech Weekly's institutional tokenization explainer, did not prescribe a specific regulatory path but framed composability as a design question with systemic implications.

On the infrastructure side, the Depository Trust & Clearing Corporation announced plans to launch a pilot transaction of tokenized RWA in July 2026, covering Russell 1000 index constituent stocks and U.S. Treasury bonds. The DTCC pilot is notable because the DTCC operates the post-trade settlement backbone for U.S. equities; its entry into tokenized RWA pilots introduces a systemically significant counterparty into a market that has so far been dominated by crypto-native issuers and bank-affiliated platforms. Whether the DTCC architecture will be designed for permissioned or permissionless circulation has not been disclosed in available materials.

Longer-range projections remain wide. Standard Chartered projects the tokenized asset market to reach $30 trillion by 2034 — a figure that implies compound annual growth of several hundred percent from current levels. Bitcoin.com News reported the tokenized RWA market reached $34.5 billion in May 2026, up over 100% year-on-year, though that figure differs from the $30 billion stabilization figure reported by PANews for the same period, reflecting methodological differences in what assets and chains are counted.

The immediate effect of the composability gap, as documented in the May 18 reporting, is that the majority of tokenized RWA value functions as a record-keeping improvement over traditional custody rather than as programmable collateral or yield-bearing DeFi liquidity. The CryptoSlate analysis does not identify a specific issuer, protocol, or regulatory change that would close the gap, nor does it establish a timeline for when compliance-constrained products might achieve DeFi integration ratios comparable to crypto-native designs. The DTCC pilot scope, the CLARITY bill's legislative status, and the IMF note's policy implications remain open questions that available sources do not resolve.