RWA Weekly — May 18, 2026

Distributed RWA value hits $33.71B for a sixth straight weekly gain, even as four of the top five chains declined and commodities surged 31% on thin activity.

Yuri Konnov

TL;DR

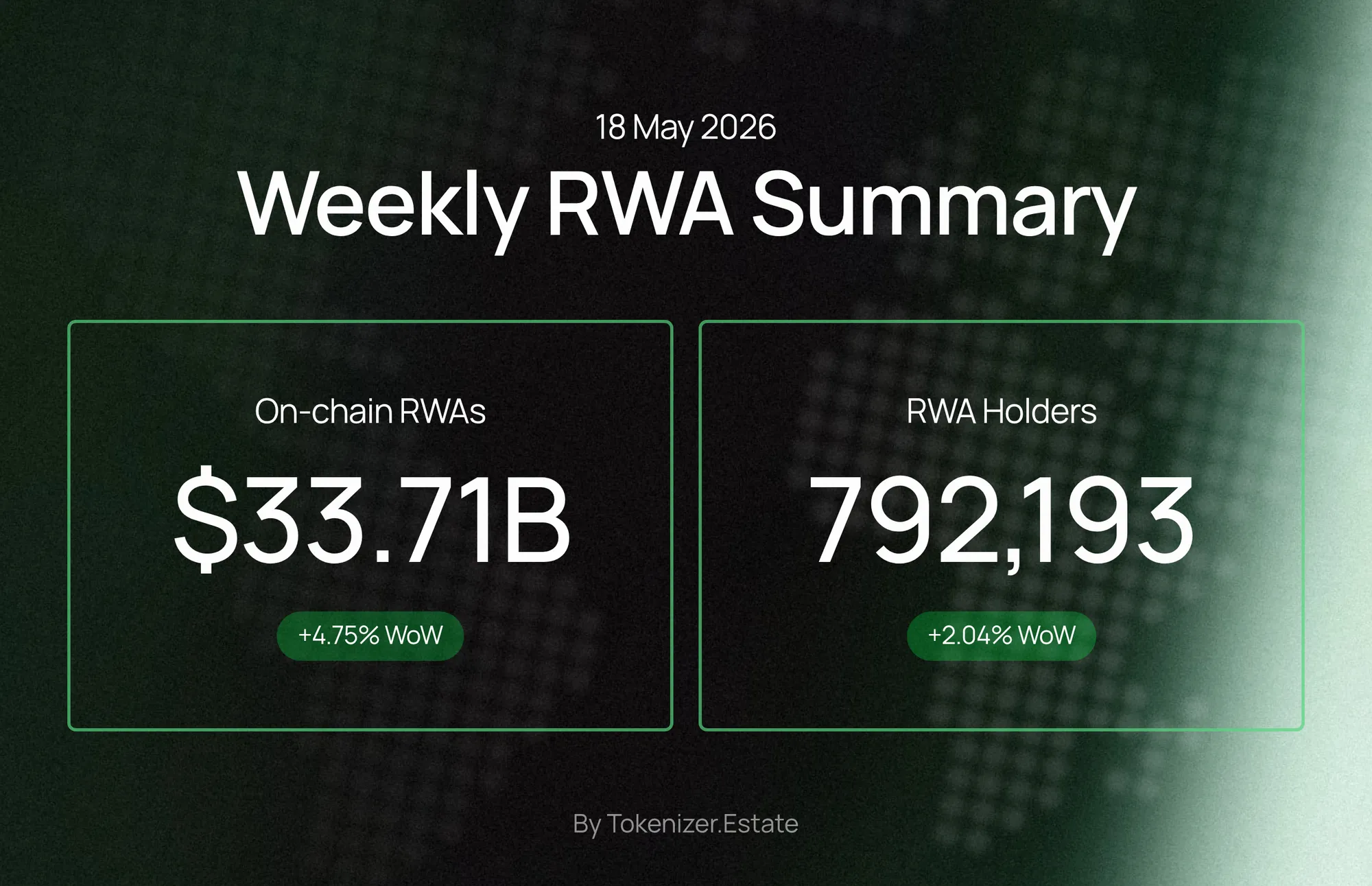

Distributed Asset Value: $33.71B — up $1.53B (+4.75%) week-over-week; accelerating, marking the sixth consecutive week of growth from $29.21B.

Total Asset Holders: 792,193 — up 15,818 (+2.04%) week-over-week; expanding, with the holder base growing steadily alongside value.

Active Networks: 35 — unchanged week-over-week; flat, holding at 35 for the period.

Stablecoin Value: $306.34B — up $2.86B (+0.94%) week-over-week; steady, continuing a measured upward drift.

Market Snapshot

Metric | Value | 7-Day Change |

|---|---|---|

Distributed Asset Value | $33.71B | +$1.53B (+4.75%) |

Represented Asset Value | $339.78B | −$30.57B (−8.25%) |

Total Asset Holders | 792,193 | +15,818 (+2.04%) |

Active Networks | 35 | +0 (0.00%) |

Stablecoin Value | $306.34B | +$2.86B (+0.94%) |

Stablecoin Holders | 253,691,653 | +1,814,878 (+0.72%) |

Distributed asset value posted a solid +4.75% gain this week, while represented asset value contracted sharply by $30.57B (−8.25%), suggesting that off-chain valuations or reporting adjustments pulled back even as on-chain distribution continued to grow. Stablecoin value moved modestly higher by +0.94%, broadly in line with the expansion in stablecoin holders (+0.72%), indicating a relatively balanced inflow dynamic on the stablecoin side.

Chain Dynamics

Chain | RWA Value | Holders | WoW Value Change |

|---|---|---|---|

Ethereum | $30.35B | 22,973,110 | +$1.57B (+5.45%) |

Solana | $16.00B | 11,886,588 | −$1.86B (−10.40%) |

Arbitrum | $14.98B | 10,138,927 | −$1.86B (−11.05%) |

BNB Chain | $13.29B | 66,077,491 | −$730.47M (−5.21%) |

Avalanche C-Chain | $9.30B | 3,143,135 | −$1.35B (−12.70%) |

Ethereum was the sole top-five chain to record a value increase this week, gaining $1.57B (+5.45%) to reach $30.35B. The remaining four chains all declined, with Avalanche C-Chain posting the steepest relative drop at −12.70%, followed by Arbitrum at −11.05% and Solana at −10.40%. This divergence reinforces Ethereum's dominant and increasingly consolidated position at the top of the RWA value rankings across the six-week historical window available.

The contrast between value and holder concentration is pronounced. BNB Chain carries the largest holder base at 66,077,491 yet holds $13.29B in RWA value, implying an average position size of approximately $201 per holder — the smallest among the top five. Ethereum, by contrast, shows 22,973,110 holders against $30.35B in value, yielding an average position of roughly $1,321. Avalanche C-Chain sits at the other extreme with 3,143,135 holders and $9.30B in value, producing an average position of approximately $2,959 — the highest in the group — indicating a more concentrated, likely institutional, holder profile.

Arbitrum and Solana present near-identical value declines of $1.86B each this week, despite differing holder bases of 10,138,927 and 11,886,588 respectively. Their average position sizes — approximately $1,477 for Arbitrum and $1,346 for Solana — are broadly comparable, suggesting similar per-holder exposure profiles even as both chains shed value at double-digit rates. The synchronised drawdown across four of the five leading chains warrants monitoring in the coming week to determine whether this reflects a broader rebalancing or chain-specific outflows.

Notable Deals This Week

South Korea FSC Greenlights Real Estate STO Plans — South Korea's Financial Services Commission has announced plans to enable security token offerings backed by multiple real estate properties, marking a significant step in the country's digital asset framework. Read more

Moody's Gives Top Rating to Fidelity, BlackRock Token Funds — Moody's has assigned its highest credit rating to tokenized money market funds from Fidelity and BlackRock, marking a major institutional validation milestone for on-chain fund products and the broader RWA tokenization sector. Read more

Grove Launches Basin DeFi Protocol for Tokenized RWAs — Grove has launched Basin, a DeFi protocol designed to provide instant on-chain stablecoin liquidity for tokenized real-world assets, with capacity of up to $1 billion in daily liquidity. Read more

Bitcoin.com and Dinari Bring Tokenized Equities Global — Bitcoin.com and Dinari have partnered to offer global investors access to more than 300 tokenized US equities and ETFs via Dinari's tokenization platform, expanding RWA access for retail and institutional participants worldwide. Read more

Kraken Parent and Franklin Templeton Eye Tokenized Yield — Payward, the parent company of crypto exchange Kraken, has partnered with Franklin Templeton to develop tokenized yield products and blockchain-based funds targeting institutional crypto markets. Read more

Commodities

Metric | Value | 7-Day Change |

|---|---|---|

Distributed Value | $7.11B | +$1.95B (+37.86%) |

Represented Value | $3.12B | +$467.98M (+17.66%) |

Total Value | $10.23B | +$2.42B (+31.00%) |

Monthly Transfer Volume | $11.05B | +$140.20M (+1.28%) |

Monthly Active Addresses | 30,185 | −1,172 (−3.74%) |

Holders | 223,114 | +522 (+0.23%) |

The commodities segment recorded a sharp jump in total value, rising $2.42B (+31.00%) to $10.23B, driven predominantly by a $1.95B surge in distributed value (+37.86%). This value expansion was not matched by activity metrics: monthly active addresses fell by 1,172 (−3.74%) to 30,185, while monthly transfer volume grew only modestly by $140.20M (+1.28%) to $11.05B — indicating that a smaller set of participants is transacting larger average amounts rather than broader user engagement widening.

The distributed/represented split stands at $7.11B versus $3.12B, with distributed value accounting for approximately 69.5% of total commodities value. Among top issuers, Paxos leads at $4.23B, followed by Tether Holdings at $3.22B and Justoken at $2.84B, with Ctrl Alt ($280.71M) and Pleasing Golden ($88.60M) occupying smaller but notable positions. The holder base of 223,114 grew only marginally (+522, +0.23%), reinforcing the pattern of value concentration rather than broad holder expansion.

Tokenized Real Estate

Metric | Value | 7-Day Change |

|---|---|---|

Distributed Value | $162.94M | −$435.52K (−0.27%) |

Represented Value | $285.58M | −$2.15 (−0.00%) |

Total Value | $448.52M | −$435.52K (−0.10%) |

Holders | 14,344 | −133 (−0.92%) |

Monthly Active Addresses | 981 | +59 (+6.40%) |

Assets | 78 | +0 (0.00%) |

Countries | 11 | +0 (0.00%) |

Tokenized real estate total value edged down marginally by $435.52K (−0.10%) to $448.52M, with the decline concentrated entirely in distributed value (−$435.52K, −0.27%) while represented value was essentially unchanged. The segment spans 78 assets across 11 countries, producing an average asset size of approximately $5.75M in total value per asset — a figure that underscores the mid-market, income-property orientation of the current tokenized real estate universe rather than large-scale commercial portfolios.

The holder count declined by 133 (−0.92%) to 14,344, yet monthly active addresses rose by 59 (+6.40%) to 981. This divergence — fewer holders but more active addresses — suggests that a subset of the existing holder base is becoming more engaged even as the overall participant count contracts slightly. The 981 active addresses represent approximately 6.8% of total holders, a relatively low activity ratio that points to a predominantly buy-and-hold posture among most participants.

The regulatory development reported this week — South Korea's Financial Services Commission announcing plans to enable security token offerings backed by multiple real estate properties — is directly relevant to the trajectory of this segment. If similar frameworks are adopted in additional jurisdictions, the current footprint of 11 countries and 78 assets could expand materially, though the on-chain data for this week shows no immediate impact on asset count or holder numbers.

Editor's Take

The sixth consecutive week of distributed value growth — from $29.21B on April 13 to $33.71B on May 18, a cumulative gain of $4.50B — establishes a durable upward trend that is increasingly difficult to attribute to short-term noise. What is notable this week is the internal composition of that growth: Ethereum absorbed the entire top-line gain and then some, while four of the five leading chains contracted, some sharply. This is a consolidation signal, not a broad-based rally, and it raises questions about whether value is rotating toward perceived safety or simply reflecting chain-specific liquidity conditions.

The commodities segment's 31% single-week value surge, set against declining active addresses, is a structural anomaly worth watching — large value moves without commensurate user activity can reflect mark-to-market adjustments or concentrated issuer activity rather than genuine market depth. Meanwhile, the Moody's top-rating assignment to Fidelity and BlackRock tokenized money market funds and the Payward-Franklin Templeton partnership signal that institutional infrastructure around on-chain yield is maturing at the product and credit-rating level, which may eventually translate into holder and value growth in segments beyond commodities. The key questions for next week: will the four declining chains stabilise or continue to cede ground to Ethereum, and will the commodities value surge be sustained by a corresponding recovery in active addresses?