Tokenized RWA Market Surges 589% Since Early 2025

A Binance research report from June 2026 reveals active tokenized real-world assets grew nearly 600% since early 2025. Tokenized stocks emerged as the fastest-growing segment, defying broader crypto market headwinds and signaling strong institutional adoption.

Yuri Konnov

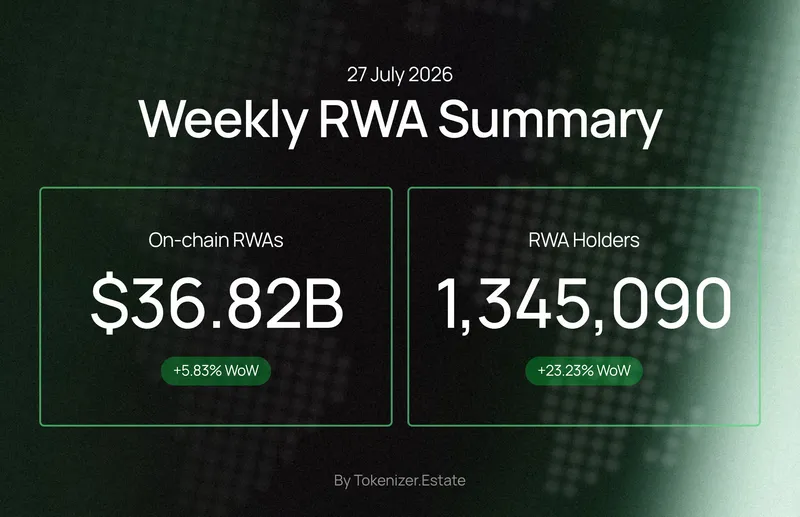

Binance Research's June 2026 Monthly Market Insights report documented that active tokenized real-world assets reached approximately $31.8 billion in total market value by early June 2026, a 589% increase from levels recorded at the start of 2025. The figure arrived as the broader crypto market contracted, with total crypto market capitalization falling 3.3% in May 2026 to $2.55 trillion amid inflation concerns, rising bond yields, and ETF outflows — making the RWA segment's expansion one of the few areas of sustained institutional momentum during the period.

Tokenized stocks emerged as the fastest-growing segment by percentage within the RWA category, rising 422% over the measured period. Tokenized bonds and money market funds added $6.5 billion in absolute value, representing 83% growth, while tokenized precious metals contributed an additional $1.5 billion, a 39% gain. Tokenized gold briefly exceeded $6 billion in January and February 2026 before retracing. The report characterized 2026 as marking a transition from a Treasury-dominated RWA market into a more diversified yield ecosystem spanning equities, credit, and commodities.

Two platforms drew specific attention in the Binance Research findings. Ondo Global Markets, which offers tokenized stocks and ETFs, surpassed $1 billion in total value locked within eight months of launch. Kraken's tokenized equities platform xStocks exceeded $25 billion in cumulative trading volume over the same eight-month window. Both figures underscore how equity tokenization, rather than fixed income, drove the segment's outsized percentage growth during the period covered by the report.

Institutional participation extended well beyond those two platforms. BlackRock, Franklin Templeton, JPMorgan, and Fidelity each launched or expanded tokenized products during the period, according to the Binance Research findings. On the infrastructure side, The Clearing House announced plans for a tokenized deposit network, and DTCC disclosed a tokenized securities pilot program scheduled to begin in July 2026, with a broader launch expected in October 2026. Those developments reflect the degree to which post-trade and settlement infrastructure has begun to accommodate on-chain asset representation alongside product-level launches from asset managers.

Regulatory developments provided a parallel track of support. The GENIUS Act, passed in 2025, established a federal framework for stablecoins. The CLARITY Act, anticipated in 2026, is expected to address the broader digital asset classification question. Together, the two pieces of legislation gave compliance officers and fund managers clearer parameters within which to structure tokenized product offerings, particularly for instruments that combine on-chain settlement with regulated securities exposure. The FXStreet coverage of the Binance report noted that the regulatory backdrop was cited as a contributing factor to institutional confidence in the segment.

The Binance Research report does not break down the $31.8 billion total by individual blockchain network, nor does it identify the specific custodial or legal structures underpinning each asset class within the aggregate figure. It does not disclose the methodology used to define "active" tokenized RWAs, which affects how the 589% growth figure should be interpreted relative to other market trackers that apply different inclusion criteria. The report also does not specify what portion of the $6.5 billion in bond and money market fund growth came from net new issuance versus price appreciation in underlying assets.

The immediate effect of the Binance Research publication is a documented, sourced benchmark for the tokenized RWA market's scale and composition as of June 2026. What it does not establish is the distribution of that $31.8 billion across jurisdictions, the secondary-market liquidity available to holders of those instruments, or whether the institutional names cited — BlackRock, Franklin Templeton, JPMorgan, Fidelity — contributed materially to the 589% growth figure or represent a smaller share of the total than the equity tokenization platforms driving the headline percentage.