RWA Weekly — June 8, 2026

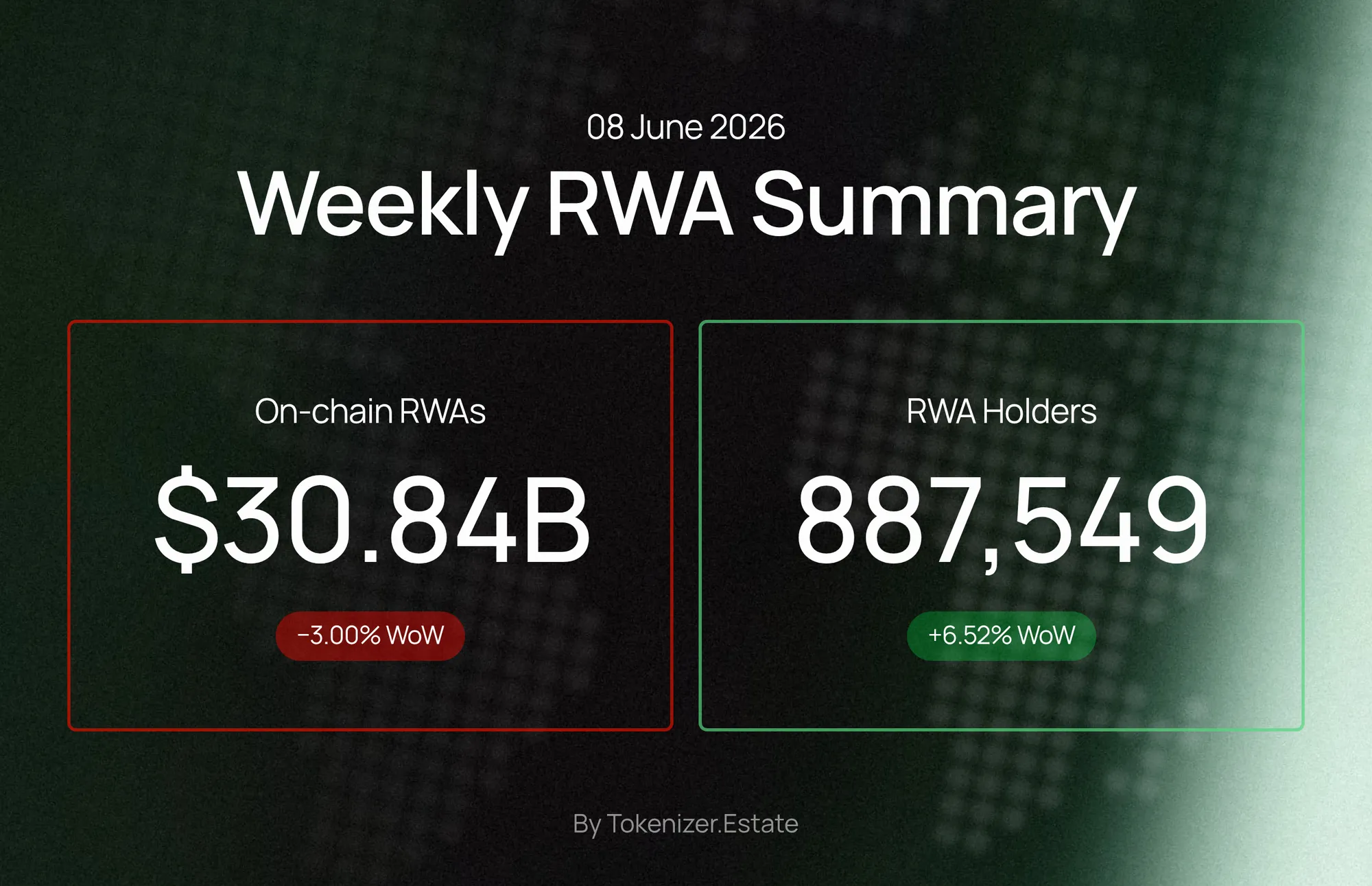

Distributed RWA value fell to $30.84B (-3.00% WoW) for a second consecutive weekly decline, even as total holders surged 6.52% to 887,549.

Yuri Konnov

TL;DR

Distributed Asset Value: $30.84B — down $955.22M (-3.00%) WoW; softening.

Total Asset Holders: 887,549 — up 54,343 (+6.52%) WoW; expanding.

Active Networks: 35 — unchanged WoW; steady.

Stablecoin Value: $298.20B — down $202.45M (-0.07%) WoW; flat.

Market Snapshot

Metric | Value | 7-Day Change |

|---|---|---|

Distributed Asset Value | $30.84B | -$955.22M (-3.00%) |

Represented Asset Value | $398.59B | +$13.20B (+3.43%) |

Total Asset Holders | 887,549 | +54,343 (+6.52%) |

Active Networks | 35 | +0 (0.00%) |

Stablecoin Value | $298.20B | -$202.45M (-0.07%) |

Stablecoin Holders | 262,822,137 | +2,647,792 (+1.02%) |

Distributed RWA value contracted by 3.00% while represented asset value expanded by 3.43%, suggesting that off-chain valuations of underlying assets moved in the opposite direction to on-chain distributed supply this week. Stablecoin value was essentially unchanged (-0.07%), while stablecoin holder counts continued to grow at a measured 1.02%, indicating that stablecoin adoption is broadening without a corresponding increase in aggregate capital deployed.

Chain Dynamics

Chain | RWA Value | Holders | WoW Value Change |

|---|---|---|---|

Ethereum | $27.72B | 23,877,989 | -$848.66M (-2.97%) |

Solana | $15.45B | 12,486,048 | -$525.02M (-3.29%) |

Arbitrum | $14.33B | 10,335,923 | -$306.44M (-2.09%) |

BNB Chain | $12.73B | 69,308,659 | -$571.36M (-4.29%) |

Avalanche C-Chain | $8.76B | 3,089,940 | -$156.72M (-1.76%) |

All five chains in the top tier recorded week-on-week value declines, with BNB Chain posting the steepest percentage drop at -4.29% and Avalanche C-Chain the shallowest at -1.76%. Ethereum retained its position as the largest chain by distributed RWA value at $27.72B, a lead it has maintained across all six historical snapshots available in this dataset — from $31.12B in the week of May 6 through to the current reading.

A notable divergence exists between value concentration and holder distribution. BNB Chain holds $12.73B in RWA value yet accounts for 69,308,659 holders, producing an average position size of approximately $184 per holder — by far the smallest among the five chains. Ethereum, by contrast, carries $27.72B across 23,877,989 holders, implying an average position of roughly $1,161. Arbitrum sits at approximately $1,386 per holder ($14.33B across 10,335,923), while Solana comes in near $1,237 ($15.45B across 12,486,048). Avalanche C-Chain's average is approximately $2,834 ($8.76B across 3,089,940 holders), the highest of the five.

The uniform direction of value declines across all five chains suggests broad-based selling or redemption pressure rather than rotation between networks. Despite the value contraction, the overall holder count at the market level rose by 54,343 this week, indicating that new participants continued to enter the market even as aggregate on-chain value declined — a pattern worth monitoring in the coming weeks.

Notable Deals This Week

ECB Launches Appia Group for Wholesale DLT Settlement — The European Central Bank has opened a call for participants in the Appia contact group, an initiative to design wholesale DLT-based settlement infrastructure for European financial markets. Read more

Mantle RWA TVL Climbs 27% to $247.5M in Q1 2026 — Mantle's RWA TVL grew 27.4% quarter-over-quarter to $247.5 million in Q1 2026, according to Messari, driven by Maple Finance's syrupUSDT product. Read more

Integra Picks SettleMint for Real Estate Tokenization — Dubai-based Integra has selected SettleMint as its digital asset lifecycle infrastructure partner, targeting real estate tokenization in the UAE and United States markets. Read more

Goldman Sachs Launches Tokenized Real Estate Fund — Goldman Sachs has partnered with Apex, Archax, Ownera, and LRC Group to launch a blockchain-native tokenized real estate fund, marking a significant step in institutional on-chain RWA adoption. Read more

CoinDesk: CLARITY Act Stall Leaves Average Americans Without Crypto Market Access — CoinDesk's Crypto Long & Short newsletter examined the stalling of the CLARITY Act and its downstream effects on ordinary American consumers' ability to participate in digital asset markets. Read more

Commodities

Metric | Value | 7-Day Change |

|---|---|---|

Distributed Value | $4.84B | -$255.07M (-5.01%) |

Represented Value | $3.14B | -$27.99M (-0.88%) |

Total Value | $7.98B | -$283.07M (-3.43%) |

Monthly Transfer Volume | $6.25B | -$789.97M (-11.22%) |

Monthly Active Addresses | 40,068 | +2,507 (+6.67%) |

Holders | 238,131 | +1,511 (+0.64%) |

Top Issuers by Total Value

Issuer | Total Value |

|---|---|

Tether Holdings | $3.08B |

Justoken | $2.86B |

Paxos | $2.00B |

Ctrl Alt | $280.71M |

Pleasing Golden | $84.43M |

Monthly transfer volume fell sharply by 11.22% to $6.25B, a decline that significantly outpaced the 3.43% contraction in total value — indicating that trading and settlement activity slowed more than the underlying asset base. Despite this, monthly active addresses rose 6.67% to 40,068 and holders grew a modest 0.64% to 238,131, suggesting that a broader but less active participant base is holding commodities positions. The distributed segment ($4.84B) continues to outweigh the represented segment ($3.14B), with distributed value accounting for approximately 60.7% of total commodities value.

Tokenized Real Estate

Metric | Value | 7-Day Change |

|---|---|---|

Distributed Value | $177.37M | -$51.01K (-0.03%) |

Represented Value | $279.84M | +$79.60 (+0.00%) |

Total Value | $457.21M | -$50.93K (-0.01%) |

Holders | 16,417 | +27 (+0.16%) |

Monthly Active Addresses | 1,227 | +84 (+7.35%) |

Assets | 90 | +0 (0.00%) |

Countries | 11 | +0 (0.00%) |

The tokenized real estate segment spans 90 assets across 11 countries, with a total value of $457.21M. At that asset count, the average asset size is approximately $5.08M per property — a figure that reflects a market still oriented toward institutional-grade or commercial assets rather than fractional retail holdings. The distributed segment ($177.37M) represents roughly 38.8% of total value, with the represented segment ($279.84M) accounting for the majority, indicating that a significant portion of real estate value remains off-chain in terms of token issuance.

Holder growth was minimal at +27 (+0.16%) for the week, bringing the total to 16,417. However, monthly active addresses rose 7.35% to 1,227, a notably faster pace than holder growth. This divergence suggests that existing participants are becoming more active rather than the market attracting a large wave of new entrants. The asset count and country footprint held flat at 90 and 11 respectively, indicating no new geographies or properties were added to the on-chain registry during the period.

Two notable deals this week are directly relevant to this segment. Goldman Sachs, in partnership with Apex, Archax, Ownera, and LRC Group, launched a blockchain-native tokenized real estate fund — a development that could, over time, add institutional-scale assets to the on-chain real estate universe. Separately, Dubai-based Integra selected SettleMint as its infrastructure partner for AI and blockchain-enabled real estate tokenization targeting the UAE and United States markets. Neither transaction is yet reflected in the current week's on-chain figures, but both represent pipeline activity that warrants monitoring in subsequent reporting periods.

Editor's Take

The most consequential signal this week is the divergence between distributed value and holder count: distributed RWA value has now declined from a peak of $33.99B (week of May 25) to $30.84B — a contraction of $3.15B over two consecutive weeks — while total holders have grown from 817,502 to 887,549 over the same period. In other words, more participants are entering the market precisely as aggregate on-chain value contracts, which may reflect lower average entry prices, broader retail participation, or both.

The uniform value decline across all five top chains, combined with a sharp 11.22% drop in commodities transfer volume, points to a broad reduction in on-chain activity rather than a sector-specific or chain-specific event. Yet institutional deal flow — the ECB's Appia initiative, the Goldman Sachs real estate fund, and Integra's infrastructure partnership — continues at a pace that is structurally disconnected from short-term on-chain metrics.

The represented asset value expanding by $13.20B (+3.43%) while distributed value fell by $955.22M is a tension worth watching: it implies that the off-chain valuation of tokenizable assets is rising even as the on-chain supply of tokens contracts. Whether this gap closes through new issuance or through a correction in represented valuations will be a defining dynamic in the weeks ahead. Key questions to track: Will distributed value stabilise above $30B, or does the two-week contraction extend into a third? And will the Goldman Sachs and Integra real estate deals begin to register in on-chain asset counts and holder figures?