Is Capital Migrating From Ethereum to XRPL RWA?

The Defiant published an analysis examining whether capital is shifting from Ethereum to XRPL's real-world asset market. The report notes that card transaction clearing in regulated stablecoins is now live across XRPL, Arbitrum, and Solana.

Yuri Konnov

Mastercard's June 3, 2026 activation of stablecoin settlement across eight blockchains — including XRPL, Arbitrum, Solana, Ethereum, Polygon, Base, Canton, and Tempo — sharpened a question analysts were already asking: whether institutional capital is rotating out of Ethereum's RWA ecosystem and into the XRP Ledger. The Defiant's capital flow analysis published this week examined that question directly, arriving at a cautious but data-supported answer.

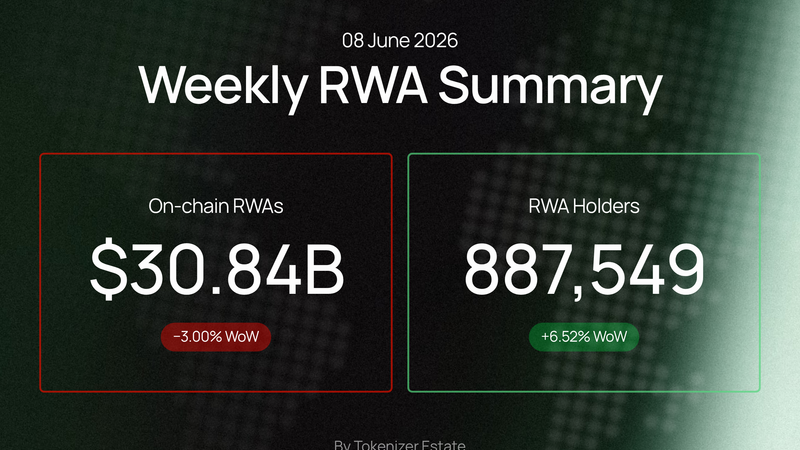

Tokenized assets on XRPL reached approximately $2.25 billion, according to Crypto.news, after the ledger's real-world asset market cap grew by more than 124% during the first quarter of 2026. That growth came off a base that stood well below $1 billion at the start of the year, making the absolute gain as notable as the percentage. An unaffiliated crypto analyst posting under the handle Ledger Man claimed that XRPL recorded approximately $1.5 billion in new RWA inflows over the 30 days preceding the analysis, while Ethereum experienced roughly $1.2 billion in outflows over the same window. Crypto.news, which reported the claim, noted it was not independently confirmed by on-chain data providers.

The Mastercard announcement provided a concrete institutional backdrop for the flow narrative. The payment network said it was enabling 24/7 card transaction clearing in regulated stablecoins — USDC, PYUSD, RLUSD, USDG, USDP, and SoFiUSD — across all eight supported chains, with an initial rollout covering the United States and Latin America. The Mastercard stablecoin settlement announcement did not specify which stablecoin-chain pairs were live at launch versus planned for later activation, nor did it disclose transaction volume targets or minimum clearing thresholds for participating issuers.

Visa's parallel expansion added further weight to the multi-chain settlement thesis. Visa's stablecoin settlement pilot reached a $7 billion annualized run rate — up 50% since the prior quarter — and now covers nine blockchains. The company added Arc, Base, Canton, Polygon, and Tempo to its existing roster of Avalanche, Ethereum, Solana, and Stellar, according to Visa's official stablecoin settlement disclosure. The overlap between Visa's and Mastercard's newly supported chains — Base, Canton, Polygon, and Tempo appear on both lists — suggests the two networks are converging on a common multi-chain settlement layer rather than pursuing differentiated infrastructure strategies.

For XRPL specifically, the Mastercard integration creates a direct link between card-rail settlement and the ledger's existing RWA tokenization infrastructure. Ripple's RLUSD stablecoin is among the six instruments Mastercard named, giving XRPL-native RWA issuers a settlement path that runs from tokenized asset to card network without leaving the ledger's native environment. Ethereum-based RWA platforms can access the same Mastercard rails, but they do so through Ethereum's settlement layer rather than through a chain where RWA issuance and card clearing share the same native infrastructure.

Several material facts remain undisclosed. Mastercard has not published the haircut or collateral treatment applied to each stablecoin during settlement, the maximum daily clearing volume per chain, or the legal entity structure governing cross-border transactions in Latin American jurisdictions. The Ledger Man inflow and outflow figures cited by Crypto.news have not been corroborated by rwa.xyz, DeFiLlama, or any named on-chain data provider, and the methodology behind the 30-day window calculation was not described. It is also unclear whether the 124% first-quarter growth figure for XRPL's RWA market cap reflects gross issuance, net of redemptions, or secondary-market price appreciation on existing tokens.

What the combined announcements establish concretely is that two of the world's largest card networks have committed operational infrastructure — not pilot programs — to multi-chain stablecoin settlement, and that XRPL is included in both networks' live or near-live chain sets. What they do not establish is whether the analyst-attributed capital rotation from Ethereum to XRPL reflects durable institutional reallocation or short-term issuance activity, nor whether XRPL's $2.25 billion in tokenized assets will sustain the growth rate recorded in the first quarter once the initial wave of Mastercard and Visa integrations is absorbed by the market.