IMF Warns Tokenization May Amplify Credit Risks

The IMF has warned that the growing adoption of tokenized real-world assets could accelerate financial risk transmission. Redemption surges and negative sentiment may rapidly reduce credit availability for riskier borrowers, triggering cascading effects across markets.

Yuri Konnov

The International Monetary Fund (IMF) published a formal research note warning that the rapid expansion of tokenized real-world assets could accelerate credit and liquidity stress in ways that outpace regulators' ability to respond — a concern the fund grounded in the mechanics of programmable settlement rather than speculative scenarios. Authored by Tobias Adrian, the IMF's Financial Counsellor and Director of the Monetary and Capital Markets Department, the note titled Tokenized Finance was covered by Forbes and other financial outlets through early June 2026.

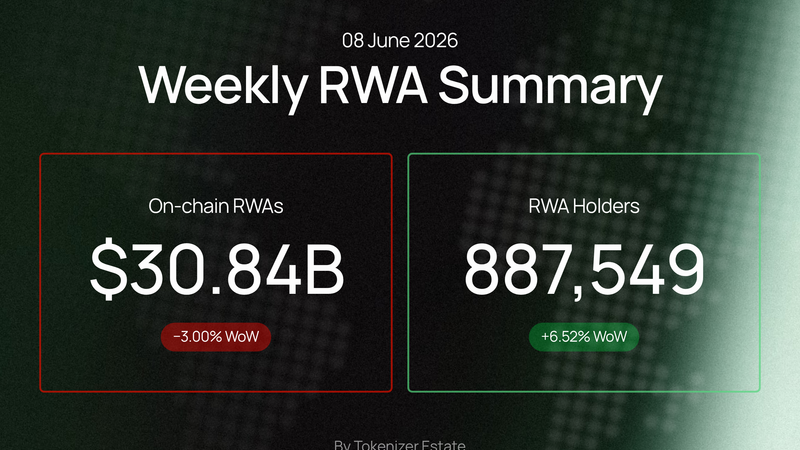

The report's scope is deliberately institutional: it focuses on RWA tokenization within regulated financial systems — banks, financial market infrastructure, and asset managers — rather than on retail crypto markets. Its central concern is that the same mechanisms that make tokenization operationally efficient also remove the temporal buffers that have historically given supervisors room to act. According to CoinDesk's coverage of the IMF findings, real-world assets on blockchain rails had already topped $23.2 billion at the time of the report, based on DeFiLlama data, with the majority concentrated in tokenized gold and money market funds.

The IMF's core technical argument centers on what it calls "atomic settlement" — the near-instantaneous finality that tokenized systems enable. While the fund acknowledges this could reduce counterparty risk and force more disciplined real-time liquidity management, it warns the same feature eliminates the processing delays that traditionally allow discretionary intervention. "Stress events are likely to unfold faster, leaving less time for discretionary intervention," the report states. Smart contracts that automatically trigger margin calls or liquidations during market downturns were specifically identified as a mechanism that could accelerate selloffs, and the fund concluded that tokenization could amplify volatility through automated markets more broadly.

The credit transmission concern is direct: negative sentiment or a surge in redemption requests could rapidly reduce credit availability for riskier borrowers, with cascading effects that move at machine speed rather than the pace of human decision-making. The IMF's note, available through the IMF's e-library, frames this not as a hypothetical but as a structural feature of programmable finance that supervisors must account for in their oversight frameworks. The report states that when trading, settlement, custody, and compliance are embedded in code, supervision must extend beyond market participants to the design, governance, and resilience of the underlying market infrastructures themselves.

The fund also identified an unresolved question at the foundation of tokenized markets: which settlement asset should underpin transactions. The IMF outlined three competing models — tokenized commercial bank deposits, regulated stablecoins, and wholesale central bank digital currencies (wCBDCs) — and did not declare a preferred outcome, noting that the choice carries significant implications for monetary policy transmission and financial stability. The absence of a settled answer on this question means that the credit and liquidity risks the report describes remain structurally embedded in current market design.

The IMF's analysis did not produce binding regulatory obligations for any jurisdiction, and the report does not identify specific tokenized products, issuers, or platforms as sources of imminent risk. It does not establish a timeline for policy action, name which standard-setting bodies — such as the Financial Stability Board or the Basel Committee on Banking Supervision — are expected to act first, or specify what regulatory thresholds would trigger intervention. The note functions as a research-based risk assessment, not a directive.

The immediate effect of the publication is that the IMF has formally placed RWA tokenization risk on the agenda of regulated financial system oversight, with a named senior author and a documented analytical framework. What the report does not establish is any concrete supervisory requirement, jurisdiction-specific rule change, or coordinated response from prudential regulators — leaving compliance officers and fund managers operating tokenized RWA products without specific new obligations arising directly from this document.