Table of Contents

TL;DR

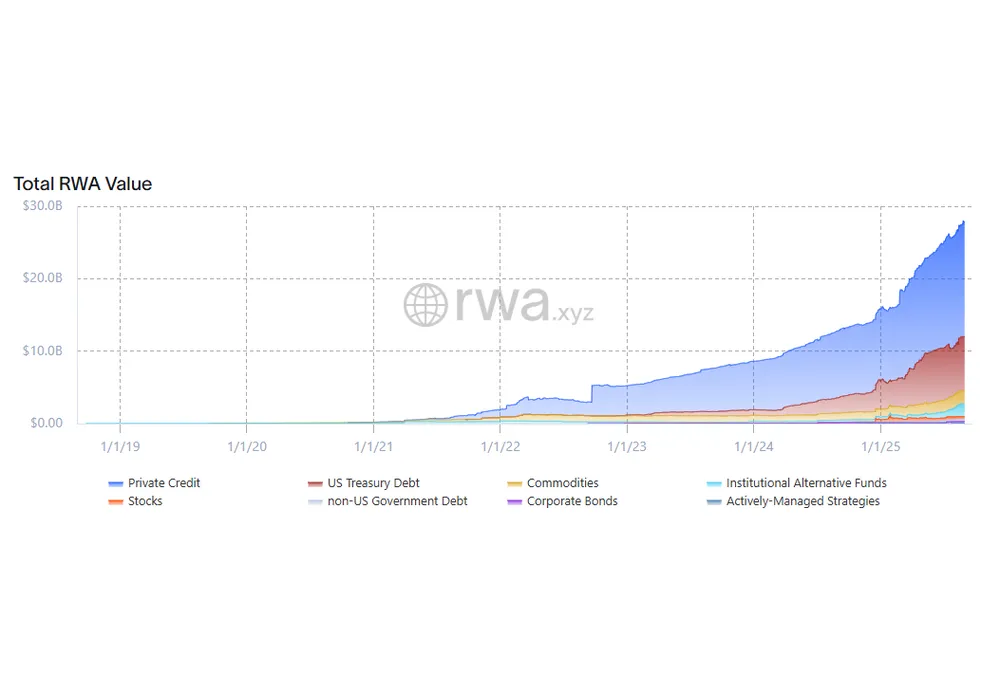

- Total on-chain RWAs: $27.92 B, up 7.3% in 30 days.

- Holders: 372,292, another 8.8% jump—participation keeps widening.

- Tokenized Treasuries: ≈$7.1 B; Circle’s USYC and WisdomTree’s funds pull in fresh assets while BlackRock’s BUIDL stays king.

- Private-credit lane: active loans edge to ≈$15.9 B at ~10% APR—still the yield magnet.

- Chains: Ethereum extends dominance, but BNB Chain’s RWA TVL more than doubles; Stellar and XRP Ledger also accelerate.

Bottom line: the market just posted its best month since March—growth is broad-based, multi-chain, and driven by a mix of “cash-like” wrappers and higher-yield credit pools.

Market snapshot (as of 1 Sep 2025)

Stablecoins again outpace RWAs in absolute dollars added, reinforcing the liquidity rails that underpin subscriptions, redemptions, and settlements.

Treasuries: rotation, not retreat

Estimated tokenized-Treasury float now sits just above $7 B (sum of top Treasury wrappers). Flows show clear rotation:

- Momentum gainers

- Circle USYC +42% MoM to $539 M.

- WisdomTree’s WTGXX +78% → $881 M despite a one-week pullback.

- Libeara’s micro-fund ULTRA +219% → $75 M—small but eye-catching.

- Soft spots

- BlackRock BUIDL –0.8% but still towers at $2.40 B—one-third of the category.

- Benji BENJI barely grows (+7%) vs. last month’s decline, suggesting some recycling into Circle/WisdomTree wrappers.

Takeaway: investors aren’t leaving treasuries—they’re arbitraging cost, yield, and on-chain integration across wrappers.

Private credit & structured yield

RWA.xyz now tracks ≈$15.9 B in live private-credit pools (up ~2% on the month, extrapolated from platform growth). Average headline APR remains near 10%, keeping these pools the gravity center for yield seekers. Centrifuge’s JAAA AAA CLO fund illustrates the momentum: +182 % MoM to $705 M AUM.

Goldfinch, Clearpool, and Tradable pipelines remain loaded; watch for an issuance spike once Q3 loans close.

Chain dynamics

Interpretation: Ethereum still anchors issuance and secondary liquidity. zkSync’s stall hints that private-credit deals paused for month-end audits. BNB Chain’s 2× jump came largely from one mid-sized Treasury wrapper launch—sustainability is the question.

Flows & investor behaviour

- Top transfers were dominated by gold tokens (XAUT, PAXG) and Circle’s USYC—suggesting portfolio hedges and fresh dollar inflows respectively.

- Holder count rose slower than in July but still high-single-digit, confirming sticky growth.

- Issuer count hit 272; small but steady rise implies few exits and continued onboarding.

What to watch in September

- BNB Chain durability: does TVL consolidate above $350 M or fade?

- Treasury spread compression: if Circle/WisdomTree keep gaining, expect fee cuts or incentive tweaks from incumbents.

- Private-credit issuance window: Goldfinch and Tradable have pools queued; a ~$500 M issuance burst would re-ignite zkSync growth.

- Commodity rotation: with gold up ~60% MoM on-chain, will oil or new ESG tokens follow suit?

Bottom line

RWAs just logged their best month since spring. Growth is broad—spanning treasuries, credit, and commodities—and multi-chain. Treasuries remain the “risk-free” anchor while private-credit pools keep the double-digit yield narrative alive. With stablecoin liquidity rising in tandem, the rails are set for the next issuance wave.

Expect continued jockeying among treasury wrappers, a resumption of zkSync private-credit momentum, and more experiments on fast-growing alt-chains like BNB Chain. The story is no longer “will RWA scale?” but “which wrappers, chains, and asset classes capture the next $10 B?”

{kind=link}