Table of Contents

Methodology note: Starting this week, the headline market figure refers to Distributed Asset Value from RWA.xyz — i.e. on-chain real-world assets excluding stablecoins and internal wrappers. Previous issues used a broader “Total RWA Value”, which also counted wrapped positions and underlying stablecoins, so the nominal number now looks lower, but the underlying market trend is unchanged.

TL;DR

- On-chain RWAs (distributed asset value) stand at $18.40B, down 0.75% over 30 days, signalling a light retrace below recent highs rather than a break in the broader on-chain RWA trend.

- Participation keeps widening: there are 560,988 asset-holding addresses (+5.86% MoM) and roughly 250 issuers (flat vs late November), so breadth continues to improve even as some legacy products wind down or merge.

- Stablecoin rails deepen: $302.07B in stablecoins (+0.96% MoM) held by 207.44M addresses (+3.03%) keeps the RWA:stablecoin ratio near 1:16, confirming that fiat-linked liquidity still far exceeds what’s actually deployed into RWAs.

- Treasuries remain the anchor, but rotation is clear: BUIDL (~$2.03B, –12.47% 30D) is still the single biggest product, yet wrappers such as USYC, WTGXX, USDY, and USTB are gaining share as investors adjust around yield, fees, and chain availability instead of leaving the category.

- Private credit and carry stay at the centre of the yield narrative: tokenized credit shows $19.08B in active loans at ~10.10% average APR, and Maple’s syrupUSDC (~$1.49B, 5.50% 7D APY) plus syrupUSDT (~$584M) sit among the largest RWAs by value.

- Commodities remain important hedges: gold-backed tokens XAUT (~$1.63B), PAXG (~$1.43B) and XAUm (~$57M) all retain meaningful distributed value and consistently appear near the top of the non-Treasury league tables.

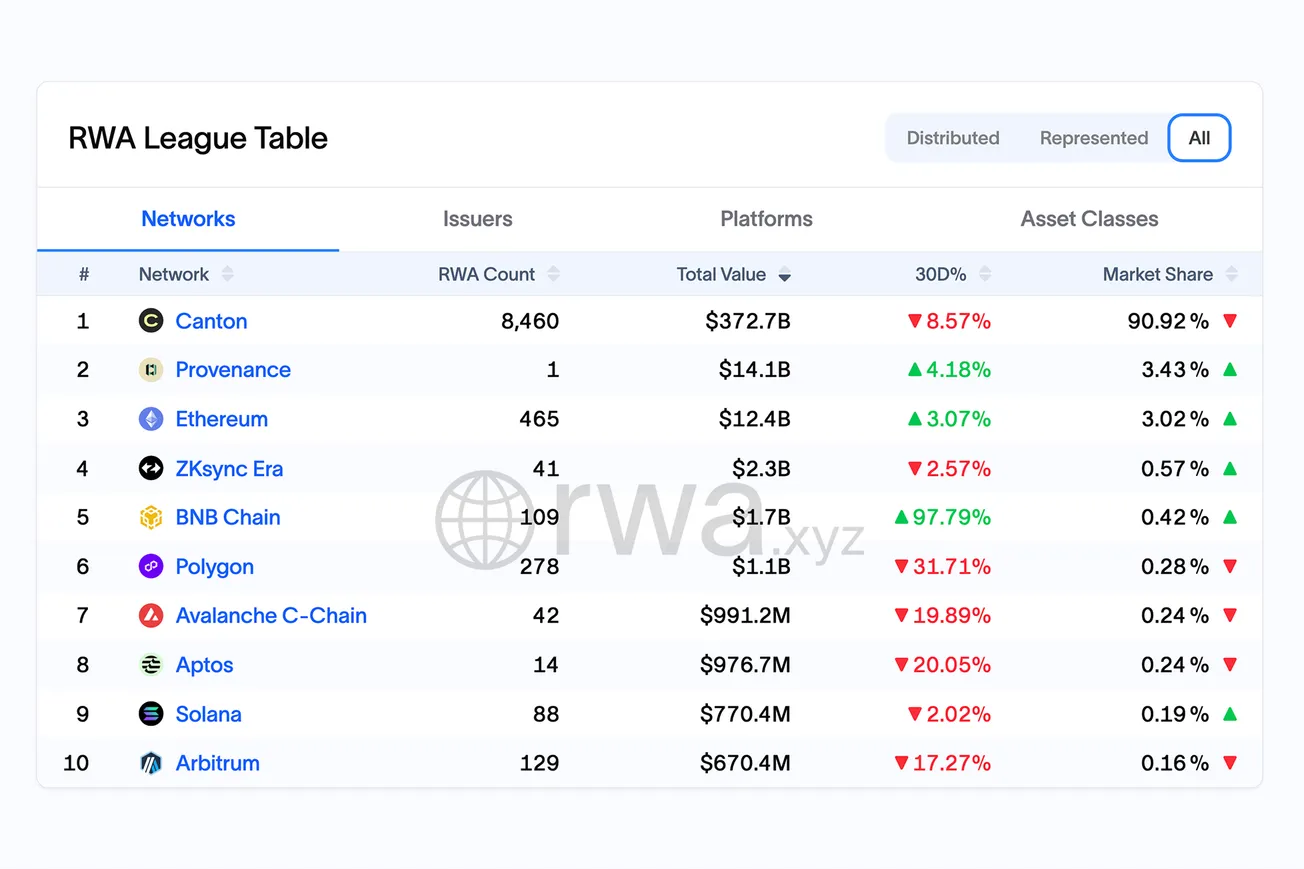

- Chains: Ethereum still leads, BNB Chain accelerates, and alt-L1s/L2s remain significant. Ethereum hosts $12.1B (≈65.7% share, +2.90% 30D) in distributed RWAs, while BNB Chain (~$1.7B, +97.79% 30D) jumps on new deployments; Solana, Avalanche, Arbitrum, Stellar, Aptos, Polygon, XRP Ledger, and zkSync Era each carry hundreds of millions in RWAs with mixed month-on-month performance.

Market snapshot (as of 8 Dec 2025)

- Total on-chain RWAs: $18.40B, down 0.75% over 30 days — a modest pullback that looks more like portfolio rebalancing after strong earlier growth than a change in direction.

- Asset holders: 560,988 (+5.86% MoM), indicating steady, organic adoption from a broad base of smaller wallets rather than one-off whale flows.

- Issuers: ≈250 active issuers, essentially unchanged from prior weeks; the small fluctuations visible in RWA.xyz data are best read as housekeeping (closures, mergers, relistings) rather than a contraction in supply.

- Stablecoins: $302.07B total value (+0.96% MoM) across 207.44M addresses (+3.03%), confirming that settlement infrastructure keeps expanding faster in user breadth than RWAs themselves and leaving plenty of stablecoin “dry powder” to back new tokenized assets.

Overall, this snapshot matches a “consolidating growth” picture: TVL cools slightly below recent highs, but user metrics, stablecoin rails, and the issuer landscape all remain on a firm upward trajectory.

Treasuries: steady core, rotating wrappers

RWA.xyz continues to show tokenized Treasuries and cash-equivalent funds as the largest single bucket of RWAs, but flows are clearly rotating across wrappers rather than exiting government exposure.

Key points from the current league tables:

- BUIDL (BlackRock / Securitize) remains the category heavyweight at around $2.03B, but with double-digit 30-day outflows, suggesting redemptions and portfolio reshuffles instead of fresh inflows.

- USYC (Circle), WTGXX (WisdomTree), USDY (Ondo) and USTB (Hashnote) continue to grow from smaller bases, booking single- to low-double-digit MoM gains as they integrate into multi-chain and DeFi workflows.

- The overall Treasury float across RWA products remains high relative to the rest of the market, but it is more fragmented: multi-chain wrappers and DeFi-native integrations increasingly compete with the earliest large funds.

Net effect: Treasuries keep their role as the “risk-reduced base layer” in RWA portfolios. The main question for December is not whether investors still want tokenized government debt — they clearly do — but which specific funds, wrappers, and chains capture incremental flows.

Private credit and carry: yield engine still on

Private credit and structured carry strategies remain the primary source of yield premium in the RWA stack.

According to RWA.xyz’s credit dashboard:

- Active loans: $19.08B

- Total loans originated: $34.59B

- Average APR: ~10.10%

- Loans outstanding: 2,864, across 10 major platforms including Figure, Tradable, Maple, PACT, Intain, Centrifuge, Goldfinch, MB, Credix, and TrueFi.

Within the token view:

- syrupUSDC (Maple) holds around $1.49B in distributed value with ~5.50% 7-day APY, putting it near the top of all RWA tokens by size.

- syrupUSDT adds another ≈$584M of credit exposure, also in mid-single-digit APY territory.

Yields in leading pools remain noticeably above short-term Treasuries, typically in mid-single to low-double digits, which explains why this segment continues to see sticky demand from institutional and high-net-worth wallets even as overall RWA TVL moves sideways.

Commodities and tokenized risk assets

Gold-backed RWAs stay central in the “on-chain hedge” toolkit:

- XAUT (Tether Gold) – $1.63B, -0.45% 7D, +4.73% 30D

- PAXG (Paxos Gold) – $1.43B, +1.33% 7D, +7.41% 30D

- XAUm (Matrixdock) – $57.2M, -0.40% 7D / 30D

Movements here still reflect underlying gold-price dynamics more than structural changes in token usage. Even with modest price fluctuations, gold RWAs remain among the largest non-Treasury assets, frequently showing up in the top-transfer lists alongside credit vaults.

Tokenized stocks and index trackers contribute an additional “risk asset” layer:

- EXOD (Backed fund) – $131.3M (-11.56% 30D)

- TSLAx, NVDAx, GOOGLon, SPYon, QQQon – mid-tens of millions each, with mixed monthly performance but steady transfer activity.

These instruments are still small relative to Treasuries and gold, but they illustrate the direction of travel: more of the traditional ETF and equity universe is being mirrored on-chain in regulated wrappers.

Chain dynamics: multi-chain as the default

RWA.xyz’s Networks league table for distributed RWAs (excluding stablecoins) confirms that the market is structurally multi-chain, with Ethereum still at the centre.

- Ethereum remains the primary venue for high-value institutional RWAs — major Treasury funds, large credit pools, and institutional vehicles.

- BNB Chain’s near-doubling in 30 days highlights how quickly RWA TVL can grow when tokenized funds and credit products plug into a retail-heavy, exchange-adjacent ecosystem.

- Solana, Avalanche, Arbitrum, Polygon, Aptos and others are going through a “two steps forward, one step back” phase: they give back part of November’s gains, but RWA stacks remain sizable, and the overall footprint stays diversified.

The pattern suggests that RWA deployment is increasingly optimized per chain (who the users are, which products they want) instead of defaulting to a single network.

Capital flows & portfolio positioning

RWA.xyz’s recent 7-day transfer data in the $0–100K band shows capital rotating across the full stack rather than clustering in a single niche. Treasury and MMF wrappers such as WTGXX and USTBL still see repeated ~$100K tickets on Ethereum and Arbitrum, signalling day-to-day liquidity and cash-management use. At the same time, income and credit products like ONyc and syrupUSDC register similar-sized moves, and even tokenized equities such as GOOGLon on BNB Chain appear in the same bracket. Put together with rising holder counts and broadly stable aggregate TVL, this points to wallets rebalancing between wrappers, chains, and risk levels, not rushing en masse into or out of RWAs.

Late-December watchlist:

- Treasury pecking order: whether flows continue to reshuffle TVL from early leaders like BUIDL toward newer wrappers from Circle, WisdomTree, Ondo, Hashnote and others.

- Next leg in private credit: if fresh issuance and new pools can lift active tokenized loans above the current ~$19B zone and keep the yield story front and centre.

- Network share and product mix: how long BNB Chain can sustain its recent RWA growth, and whether tokenized equities and structured funds start to claim a visibly larger slice of total TVL across non-Ethereum networks.

Overall, as of December 8, the RWA market looks much closer to a core fixed-income and credit stack with multi-chain delivery than to an experimental niche: growth is slower but steadier, participation keeps broadening, and the building blocks — treasuries, private credit, gold, and stablecoins — are firmly established on-chain.

{kind=link}