RWA Weekly — December 15, 2025

RWA news for December 15: on-chain RWAs stabilize just under $19B under the new Distributed Asset Value lens, while Treasuries keep rotating between wrappers, private credit maintains ~10% yields, and gold plus tokenized stocks gradually deepen the hedge-and-beta layer.

TL;DR

- On-chain RWAs (distributed asset value) stand at $18.61B, up 0.78% over 30 days, pointing to a slow, carry-driven grind higher after the November reset rather than a new explosive leg.

- Participation keeps widening: 571,857 asset-holding addresses (+6.13% over 30 days) and roughly 240–250 issuers mean the market keeps onboarding new wallets and platforms even as some legacy products consolidate or wind down.

- Stablecoin rails still run ahead of RWAs: $300.79B in stablecoins (+1.18% 30D) across 210.11M addresses (+3.64% 30D) keeps the RWA:stablecoin ratio near 1:16, underlining that dollar liquidity and settlement capacity are not the bottleneck.

- Treasuries remain the anchor, but leadership is now contested: tokenized Treasuries total about $8.96B (–1.58% 7D, 3.58% 7D APY), with BUIDL (~$1.8B, –9.95% 30D) trimming, while USYC, OUSG, BENJI, WTGXX, USDY, USTB and CUMIU grow or hold steady from smaller bases as investors optimise yield, fees and chain coverage.

- Private credit and carry stay at the centre of the yield narrative: there are $19.20B of active tokenized loans out of $34.93B originated, with 10.09% average APR across 2,871 loans; Maple, Figure, Tradable, PACT, Centrifuge, Goldfinch and others still offer a ladder of mid-single- to double-digit APYs.

- Commodities and tokenized risk assets quietly build out the macro + beta sleeve: gold-backed tokens XAUT ($1.7B, +2.89% 30D), PAXG ($1.5B, +2.7% 30D) and XAUm ($56.2M, +2.13% 30D) remain the main on-chain hedge layer, while equity and ETF wrappers like EXOD ($136.8M), TSLAx ($43.8M), QQQon ($20.4M), NVDAon ($15.6M, +94.19% 30D) add directional stock exposure on top.

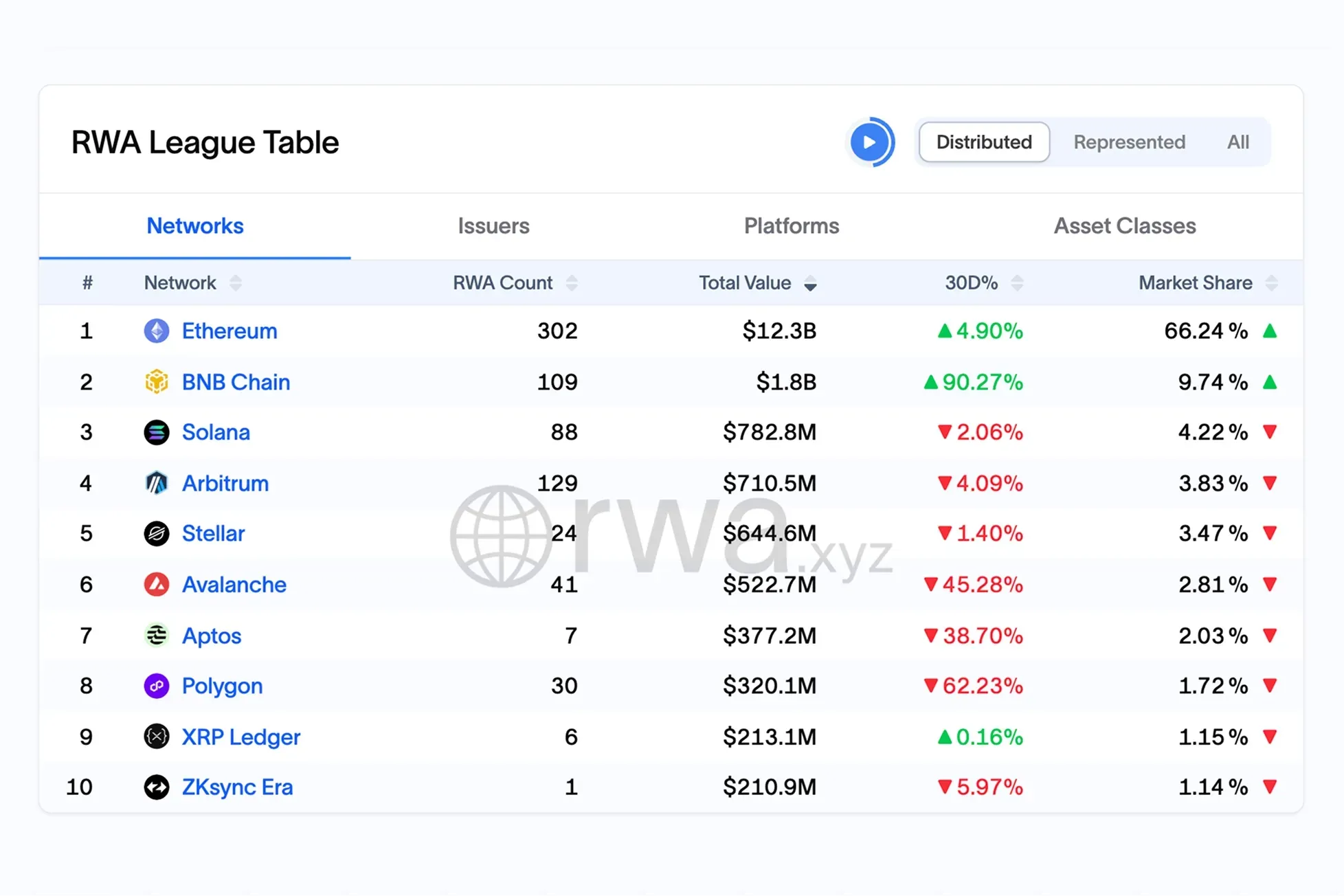

- Chains: Ethereum still leads, BNB Chain accelerates, and alt-L1s/L2s remain significant. Ethereum hosts $12.3B (≈66% share, +4.90% 30D) in distributed RWAs, while BNB Chain (~$1.8B, +90.27% 30D) jumps on new deployments; Solana, Arbitrum, Stellar, Avalanche, Aptos, Polygon, XRP Ledger and zkSync Era each carry hundreds of millions in RWAs with mixed month-on-month performance.

Market snapshot (as of 15 Dec 2025)

- Total on-chain RWAs (DAV): $18.61B, up 0.78% over 30 days — a modest uptick that fits a “slow carry expansion” profile rather than a momentum spike.

- Asset holders: 571,857 (+6.13% 30D), showing that user breadth continues to outpace value, with more wallets holding RWAs even though headline TVL moves only slightly.

- Issuers: around 240+ active issuers on RWA.xyz, essentially flat versus late November; small changes mostly reflect housekeeping (closures, relistings, mergers) rather than a structural retreat in supply.

- Stablecoins: $300.79B total stablecoin value (+1.18% 30D) across 210.11M addresses (+3.64%), confirming that settlement rails continue to deepen in breadth faster than RWAs themselves.

Overall, the picture is of a maturing carry market: TVL edges higher, user counts grow more quickly, and the plumbing — stablecoins, platforms, chains — looks solid even as capital keeps shuffling between wrappers and networks.

Treasuries: steady core, rotating wrappers

Tokenized Treasuries and cash-equivalent funds remain the largest single bucket of RWAs, with $8.96B in value as of December 15, –1.58% over 7 days, and a composite 7-day APY of 3.58%.

Within that aggregate, leadership is clearly in rotation rather than locked in:

- Securitize / BUIDL: platform-level Treasuries around $1.9B, –27.14% 30D, with BUIDL itself at roughly $1.8B and –9.95% over 30 days. It is still one of the single largest RWA positions, but also the main donor of capital rotating into other wrappers.

- Circle (USYC): roughly $1.3B, +4.7% 30D, distributed across Ethereum, Solana, NEAR and BNB Chain, and increasingly used as “yielded USDC” in DeFi and treasury management.

- Ondo (OUSG / USDY): combined ~$1.5B on the Treasuries dashboard; OUSG sits around $822.6M (+6.45% 30D) and USDY near $702.6M (+0.05% 30D), with USDY held by more than 16k addresses, making it one of the most widely held yield-bearing RWAs.

- Libeara & Franklin Templeton: Libeara’s non-US government funds add ~$840M+ in aggregate, while BENJI from Franklin Templeton stands near $818.9M with a marginal 30-day dip, still a flagship for regulated tokenized MMFs.

- WisdomTree & Superstate: WTGXX is around $705M with a small 30-day pullback, but now spans multiple chains (Stellar, Optimism, Plume, Ethereum, Base, Avalanche, Arbitrum). USTB sits near $602M and has one of the stronger 30-day growth profiles despite a mild week-on-week decline.

Below that, assets like CUMIU, FDIT, JTRSY and a series of niche government-debt wrappers fill out a long tail of more specialized mandates.

Takeaway: Treasuries still anchor the “risk-reduced base layer” of RWA portfolios, but the story is now about fragmentation and competition: multi-chain, DeFi-integrated wrappers are steadily chipping away at early incumbents as allocators tune for yield, fees, access and composability.

Private credit and carry: yield engine still on

Private credit and structured yield strategies remain the main source of yield premium in the RWA stack:

- Active loans: $19.20B

- Total loans originated: $34.93B

- Average APR: 10.09%

- Total loans: 2,871, across 10 major platforms (Figure, Tradable, Maple, PACT, Intain, Centrifuge, Goldfinch, MB | Mercado Bitcoin, Credix, TrueFi).

Platform-level highlights:

- Figure (Provenance): around $17.93B in total loans, $14.19B active, mostly institutional mortgages and structured finance; it remains the size anchor of tokenized credit even though much of it is represented rather than fully on public L1s.

- Tradable (zkSync Era): $5.10B total / $2.05B active, with ~11.08% base APY and no defaults recorded yet on RWA.xyz — a large, high-yield book concentrated on a single L2.

- Maple (Ethereum / Solana / Base): $6.19B total / $1.74B active, 9.19% average base APY and $47.1M in defaults, showing both scale and real credit risk.

- PACT (Aptos): $1.91B total / $596.5M active, a very high 22.31% avg. base APY and $143.7M of defaults, underlining the trade-off between double-digit coupons and realised losses.

- Centrifuge, Goldfinch, Intain, MB, Credix, TrueFi jointly add hundreds of millions in loans with APYs across the 5–18% range, often backed by real-estate, trade-finance or speciality-credit collateral.

At the token/vault level, a familiar “carry ladder” remains in place:

- syrupUSDC (Maple) with ~$892M in principal outstanding, ~6.5% APY,

- syrupUSDT with ~$684M, a bit above 5% APY,

sit alongside more specialised pools (for example, Intain’s CRE and aviation deals, high-yield PACT structures, and Goldfinch/Centrifuge real-asset pools).

Overall, credit risk is visible and priced, but the category as a whole still offers a clear yield pickup over Treasuries, and the data shows a live, rolling market — loans are being originated, refinanced and repaid, not left idle.

Commodities and tokenized risk assets

Commodities and tokenized risk assets: Gold-backed tokens like XAUT (~$1.7B), PAXG (~$1.5B) and XAUm (~$56M) remain among the largest non-Treasury RWAs, with low-single-digit 30-day gains that mainly reflect moves in the underlying metal. At the same time, a smaller but growing sleeve of tokenized equities and index trackers — EXOD (~$136.8M), TSLAx (~$43.8M), SPYon, IVVon, QQQon, NVDAon, IEFAon (mostly in the mid-tens of millions) — adds directional stock and ETF exposure on-chain. In combination, this creates a two-part role in portfolios: gold as the macro hedge and equity wrappers for risk-on positioning, layered on top of Treasuries and credit.

Chain dynamics: multi-chain as the default

RWA.xyz’s Networks league table (Distributed, excluding stablecoins) confirms that RWAs are now structurally multi-chain with a clear centre of gravity:

- Ethereum holds about $12.3B in distributed RWAs, +4.90% over 30 days, for 66.24% market share across 300+ assets — still the main settlement, liquidity and issuance hub for large Treasury funds, major credit pools and flagship gold/equity wrappers.

- BNB Chain has grown into a clear second pillar with ~$1.8B in distributed RWAs, +90.27% 30D, and 9.74% share across more than 100 assets, helped by tokenized stocks, structured products and DeFi-driven flows.

- Solana and Arbitrum sit in the next tier:

- Solana: $782.8M, 4.22% share;

- Arbitrum: $710.5M, 3.83% share;

both benefit from a mix of Treasury wrappers, credit vaults and tokenized stocks.

- Stellar, Avalanche, Aptos, Polygon, XRP Ledger, zkSync Era each host hundreds of millions in RWAs:

- Stellar: $644.6M, 3.47% share;

- Avalanche: $522.7M, 2.81% share (digesting a large 30-day drawdown);

- Aptos: $377.2M, 2.03% share;

- Polygon: $320.1M, 1.72% share;

- XRP Ledger: $213.1M, 1.15% share;

- zkSync Era: $210.9M, 1.14% share.

The pattern from November and early December holds: Ethereum is entrenched as the anchor, but RWAs are increasingly deployed “per chain, per use case” — retail-heavy BNB, L2 Treasury and credit on Arbitrum, experimental and high-throughput plays on Solana and zkSync, and institutional or regional niches on Stellar, Avalanche, Aptos, Polygon and XRP.

Capital flows & portfolio positioning

Looking across the latest RWA.xyz snapshots, flows still point to rebalancing within the stack rather than a one-way rush in or out:

- In Treasuries, total value is slightly lower week-on-week, but the main story is rotation between wrappers: Securitize/BUIDL gives up share while multi-chain and DeFi-friendly options from Circle, Ondo, Libeara, WisdomTree and Superstate attract incremental capital.

- In private credit, active loans and average APR are essentially unchanged, showing a rolling market with ongoing origination and repayment rather than a freeze or unwind, even as some platforms carry visible default histories.

- In commodities and tokenized stocks, gold RWAs grind higher with the metal, and equity trackers — especially NVDAon and TSLAx — remain meaningful in value and growth, suggesting that more portfolios are now using RWAs for hedge + beta, not just for cash management.

- On the network side, positive 30-day moves in Ethereum and BNB, stable-to-slightly-lower numbers on Solana and Arbitrum, and sharp drawdowns on Avalanche, Aptos and Polygon indicate redistribution across chains, not a collapse of RWA activity.

What to watch into year-end

- Treasury pecking order: whether flows settle into a more stable hierarchy between BUIDL, USYC, OUSG, BENJI, WTGXX, USDY, USTB and CUMIU, or whether fees, yields and integrations keep the leaderboard fluid.

- Credit cadence: if new private-credit deals can keep active tokenized loans around or above the current ~$19B level as year-end repayments land, and how defaults on higher-yield platforms shape investor appetite going into Q1.

- Network mix: whether BNB Chain can hold onto its rapid 30-day gains, and how quickly newer venues like zkSync Era and Base convert large represented positions and stablecoin rails into fully distributed, user-facing RWAs.