Table of Contents

TL;DR

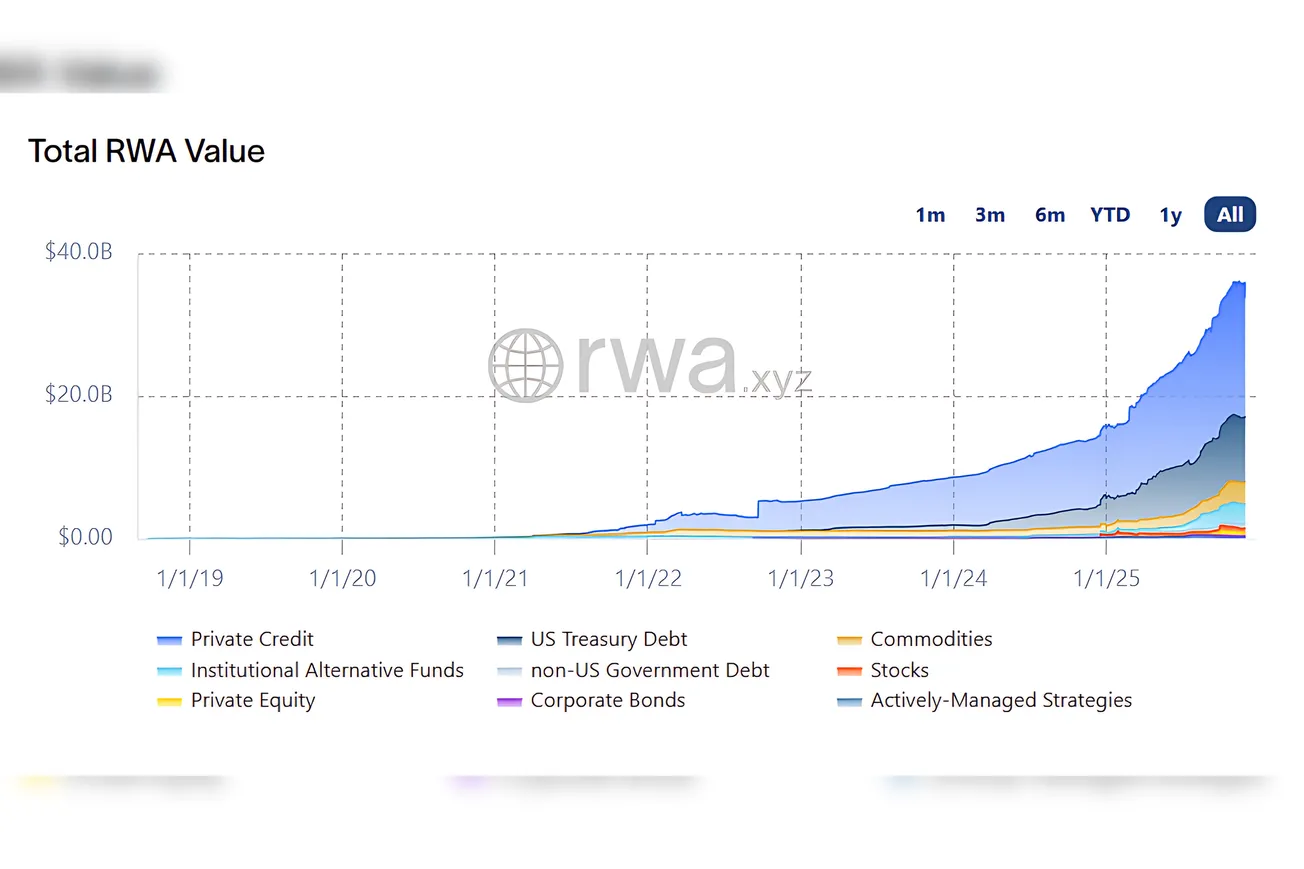

- On-chain RWAs reached $36.08B, adding 0.8% over 30 days and marking another all‑time high, but with clearly slower, more “carry-driven” growth than earlier in Q4.

- Participation keeps widening: 553,745 holders (+6.2% MoM) and 250 issuers (slightly lower after minor consolidation), showing breadth still improves even as a few legacy products shrink or merge.

- Stablecoin rails deepen: $300.73B in stablecoins (+1.11% MoM) held by 205.34M addresses (+2.78%), reinforcing the RWA:stablecoin ratio near 1:8–1:9 and underlining that liquidity is not the bottleneck.

- Treasuries remain the anchor, but rotation continues: inflows cluster in Circle‑style and Theo/WisdomTree vehicles, while some large incumbents keep bleeding modest TVL as investors optimize fees, yields, and on‑chain integrations.

- Private credit and carry strategies still define the yield narrative; institutional‑grade credit vaults and Maple‑style products retain mid‑single to low‑double‑digit APYs and feature among the largest weekly transfers.

- Commodities stay relevant as hedges: gold‑backed tokens (XAUT, PAXG, XAUm) see mixed performance but continue to appear in top transfer lists together with RWA credit and fund tokens.

- Chains: Ethereum keeps its lead in RWA value, while Avalanche, BNB Chain, Polygon, and Solana hold or extend high shares after a strong November, confirming a structurally multi‑chain market.

Market snapshot (as of 1 Dec 2025)

- Total on-chain RWAs: $36.08B, up 0.77% over 30 days — new high, but clearly slower than the early‑November and mid‑autumn bursts.

- Asset holders: 553,745 (+6.21% MoM), pointing to continued organic adoption from a long tail of smaller wallets rather than just a few whales.

- Issuers: 250, a marginal dip versus late November that likely reflects housekeeping (closures/mergers) more than deterioration in supply.

- Stablecoins: $300.73B total value (+1.11% MoM) held by 205.34M addresses (+2.78%), confirming that settlement rails still expand faster in breadth than RWAs themselves.

This snapshot fits a “maturing bull” profile: TVL grinds higher, user counts climb solidly, and infrastructure (stablecoins, issuers, chains) stays robust even as some individual products deflate.

Treasuries: steady core, rotating wrappers

RWA.xyz still shows tokenized Treasuries as the single largest category by value, but flows keep shuffling between wrappers rather than exiting the asset class.

Key themes:

- Aggregate Treasury float edges up in line with total RWAs, but dispersion grows: smaller and more DeFi‑native wrappers gain share while a few jumbo funds trim.

- Circle‑style products and money‑market‑like funds from WisdomTree/Theo continue to post meaningful MoM gains, indicating that institutional and crypto‑native treasuries still want short‑duration, highly liquid U.S. government exposure.

- The largest incumbent Treasury fund remains the category anchor, but its relative share slides as capital rotates for fee, integration, and sometimes chain‑specific reasons (e.g., moving towards wrappers available on alt‑L1s).

Net effect: Treasuries keep their status as the “risk‑reduced base layer” for RWA portfolios; the story is about which wrapper wins, not whether the asset class remains on‑chain.

Private credit and carry: yield engine still on

Private credit, structured products, and carry funds (e.g., USCC‑like strategies and Maple‑style syrup vaults) continue to act as the main yield engine in the RWA stack.

- RWA.xyz’s league tables still show several private‑credit and yield vehicles in the upper ranks by distributed value, even if MoM changes are smaller than in previous months.

- Top‑transfer lists include private‑credit and fund tickers (such as RLP, syrup‑style tokens), with many transfers clustered around the ≈$100K size — a typical institutional or high‑net‑worth order ticket, not just retail activity.

Headline APYs in major pools remain meaningfully above Treasuries, usually in mid‑single to low‑double digits, which explains why credit growth, though no longer explosive, remains persistent and sticky.

Commodities and tokenized risk assets

Commodities, especially gold, and tokenized equities continue to evolve as the “satellite” sleeve of RWA portfolios.

- Gold tokens like XAUT, PAXG, and XAUm maintain significant distributed value, and multiple XAUT transfers in the ~$100K range show that they are actively traded hedges rather than dormant stores.

- Tokenized stocks and index funds (QQQon, various xStock tickers on Solana, Ondo tokenized blue chips) appear across the league table, indicating increased comfort with listed equity and ETF exposure on‑chain.

This segment is still smaller than Treasuries and private credit but plays a clear role: macro hedging via gold, and speculative or tactical positioning via tokenized equities and ETFs.

Chain dynamics: multi‑chain as the default

| Network | RWA holders | RWA total value (excl. stablecoins) |

|---|---|---|

| Ethereum | 130,079 | $12,072,578,059 |

| BNB Chain | 3,546 | $1,618,202,906 |

| Solana | 105,705 | $766,222,522 |

| Avalanche C-Chain | 7,850 | $999,204,175 |

| Polygon | 4,134 | $1,436,265,169 |

RWA.xyz’s RWA League Table confirms that while Ethereum remains the main hub by total distributed value, the RWA footprint is now structurally multi‑chain.

- Ethereum still hosts the bulk of high‑value institutional RWAs (funds, Treasuries, large credit pools), keeping it the primary liquidity and issuance venue.

- Avalanche, BNB Chain, Polygon, and Solana each hold substantial and growing RWA stacks, powered by combinations of institutional funds, mid‑cap Treasury wrappers, commodities, and tokenized stocks.

Relative growth rates have cooled compared to early November, but alt‑L1s continue to gain share at the margin, especially in segments like tokenized equities and niche funds, suggesting that RWA deployment is now being optimized per chain rather than defaulting to a single network.

Flows, behaviour, and what’s next

Recent top transfers on RWA.xyz feature a familiar mix:

- Gold tokens (notably PAXG and XAUT) in ~$100K clips — portfolio hedges and macro positioning.

- Credit/fund tokens (e.g., RLP, syrupUSDC) near the same ticket size — institution‑scale rebalancing into and out of yield strategies.

Taken together with rising holder counts, this suggests a market characterized by continuous re‑optimization (between wrappers, chains, and risk levels) rather than aggressive net de‑risking or frothy new inflows.

Into December, key things to watch:

- Whether Treasury rotation stabilizes and a new equilibrium emerges between Circle/WisdomTree/Theo products and legacy behemoths.

- If a fresh private‑credit issuance wave appears that could re‑accelerate growth on L2s and alt‑L1s that host many credit pools.

- How tokenized equities and niche funds perform into year‑end, especially if traditional markets stay volatile and on‑chain wrappers become an attractive 24/7 trading venue.

Overall, as of December 1, RWAs sit at record highs with slower, more sustainable growth, a broader holder base, and firmly entrenched multi‑chain infrastructure — a profile much closer to a core asset class than an emerging niche.

{kind=link}