Table of Contents

TL;DR

- On-chain RWAs sit at $26.48B, up ~4.1% over 30 days, with holders growing double digits again.

- Tokenized Treasuries remain the dominant class, totaling ~$6.9B, but dispersion is clear: Securitize and Ondo lead, while WisdomTree and Circle show sharp inflows.

- Private credit continues to command attention, with active loans near $15.7B at ~9.9% APR.

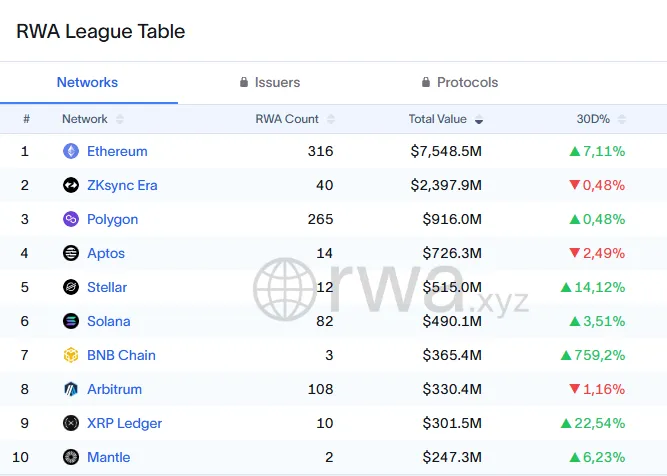

- Ethereum leads networks by value, but BNB Chain and Stellar post standout 30‑day growth, while zkSync’s momentum stalls.

Overall: the RWA base keeps firming, breadth of participation widens, and venues/platforms are segmenting between “safe yield” and “private credit alpha.”

Market snapshot (as of Aug 25, 2025)

- Total RWA on-chain: $26.48B (+4.07% vs. 30 days ago)

- Holders: 367,503 (+11.13%)

- Issuers: 268

- Stablecoins (context): $267.64B total market cap (+4.55%) across 189.99M holders

Takeaway: the macro base for RWAs is expanding steadily, supported by user growth and stablecoin liquidity rails above $260B.

Treasuries: steady growth, rotation underway

Tokenized U.S. Treasuries are now ~$6.9B, with Securitize’s BlackRock BUIDL fund still the largest single wrapper (~$2.40B market cap).

But allocations are in motion:

- Winners:

- WisdomTree’s WTGXX doubled (+89.8% over 30D) → ~$931M

- Circle’s USYC nearly doubled (+99.3%) → $517M

- Libeara’s ULTRA fund surged 142% → $52M

- Laggards:

- Franklin Benji (BENJI) softened (–4.95%) → ~$749M

- Janus Henderson JTRSY down (–12.5%)

This points to active rotation within the “cash-like” RWA segment—demand isn’t leaving Treasuries, it’s chasing better wrappers, integrations, and fee structures.

Private credit: still the growth engine

RWA.xyz tracks ~$15.7B in active loans and $28.8B originated, with prevailing APY near 9.9%.

Sectors include BNPL pools, litigation finance, SME/fintech working capital, and structured credit notes.

- zkSync still anchors a large share of private-credit flows, though growth flattened this cycle (–0.5% 30D).

- Expect more issuance pipelines (Tradable, Clearpool, Goldfinch derivatives) to bolster throughput.

Key point: yield-seeking investors are using credit rails programmatically—ticket sizes in the $20M–$250M range look increasingly institutional.

Networks & market structure

- Ethereum: $7.55B (51.7% share; +7.1% over 30D) remains dominant.

- zkSync Era: $2.40B (16.4% share; –0.5%) slows after strong prior gains.

- BNB Chain: $365M with +759% 30D growth—a breakout, though off a small base.

- Stellar +22%, XRP Ledger +22% → strong inflows into gold tokens and non‑US debt.

- Polygon & Solana add steady depth but are losing marginal share.

Signal: multi-chain distribution is converging into a “hub‑and‑spoke” model—Ethereum anchoring issuance, L2s/appchains processing niche verticals (credit, gold, corporate debt).

Flows & investors

- Holders surged +11% in 30 days → more addresses participating.

- Flows are rotating, not exiting (e.g., BUIDL dips while Circle/WisdomTree gain).

- Gold tokens (PAXG, XAUT) posted large transfers (~$100K each), underscoring renewed commodity demand alongside Treasuries.

Net: participation breadth is solid, with allocations moving within RWAs rather than outward.

What to watch next

- Treasury wrappers: Does WisdomTree’s and Circle’s momentum hold, or does BlackRock recapture flows?

- BNB Chain anomaly: Is the 7.5x jump sustainable, or a one-off liquidity injection?

- Private credit issuance: If zkSync pipelines reaccelerate, the chain could reclaim lost growth.

- Gold demand: PAXG/XAUT transfers hint at a rotation into commodities as a hedge against expected rate cuts.

Bottom line

RWAs continue to expand steadily, now above $26.4B on-chain. The market is maturing into two distinct lanes:

- “Cash-like” Treasuries (~$6.9B, competitive and fee-driven, rotating across wrappers).

- “Yield-y” private credit (~$15.7B active, institutional-sized deals, higher-risk pools).

Ethereum anchors core liquidity, while select L2s and alternative chains (zkSync, Stellar, BNB) are carving space by specializing in asset type or issuer base. With stablecoin liquidity still immense, settlement rails are primed for continued expansion.

RWAs are entering a multi-chain, multi-venue era with clear segmentation between low‑risk treasuries and higher‑yield credit, and user participation keeps rising at double-digit pace—a sign of real adoption rather than speculative churn.

{kind=link}