Table of Contents

TL;DR

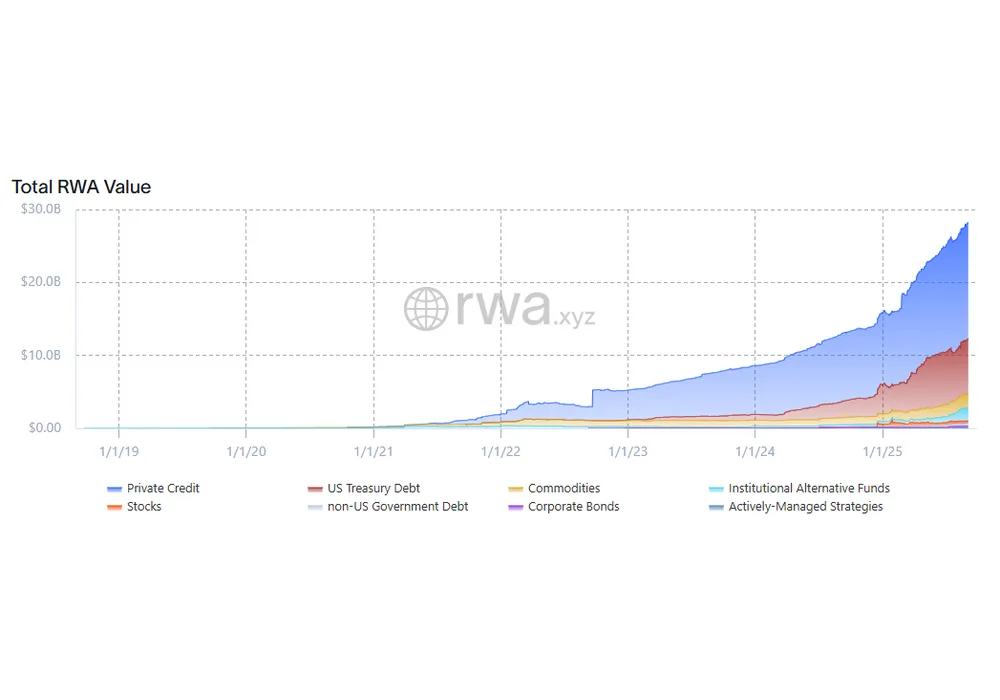

- On-chain RWA value climbs to $28.39 B (▲6.3% in 30 days) as the market logs a third straight month of growth.

- Holder count pushes past 380 K (▲8.7%), confirming widening participation.

- Tokenized Treasuries stay above $7 B but leadership shuffles: Circle’s USYC and Fidelity’s surprise FDIT launch soak up inflows while BlackRock’s BUIDL slips.

- Private-credit surge: Centrifuge’s AAA CLO fund JAAA nears $0.8 B AUM, helping push active credit above $16 B.

- Chains: Ethereum widens its lead; Avalanche and BNB Chain record the fastest month-over-month TVL jumps; zkSync growth pauses.

- Commodities re-ignite: PAXG overtakes XAUT as the largest on-chain gold token; WTGOLD mints on Stellar.

Market snapshot

| Metric | Value | 30-day Δ | Trend |

|---|---|---|---|

| Total RWA on-chain | $28.39 B | ▲6.26% | Best run since Q1 |

| Holding addresses | 380,483 | ▲8.70% | Broadening user base |

| Issuers | 274 | +2 | Pipeline alive |

| Stablecoin value (context) | $277.26 B | ▲6.58% | Liquidity rails rising |

Key message: macro growth in both stablecoins and RWAs underlines healthy on-chain liquidity for subscriptions, redemptions, and settlements.

Treasuries: rotation accelerates

Estimated float remains just over $7 B, but flows have rotated hard over the past four weeks:

- Gainers

- Circle USYC ↑9.8% MoM → $581 M

- Fidelity’s FDIT blasts onto the board at $204 M, signaling big-house competition.

- Libeara ULTRA ↑265% → $86 M on tiny base.

- Losers / cooling

- BlackRock BUIDL ↓2.0% but still towers at $2.24 B (largest single wrapper).

- WisdomTree WTGXX momentum fades after a red-hot July (still +40% over 30 days).

Interpretation: demand is not leaving Treasuries; it is arbitraging wrappers, fees, and chain integrations.

Private credit & yield products

Centrifuge steals the show:

- JAAA AAA CLO fund up 68% MoM to $756 M, becoming the sixth-largest RWA on-chain.

- Superstate’s USCC crypto carry fund gains 25% MoM to $226 M.

Total active private-credit loans now sit around $16 B with average coupons just under 10%. Appetite for institutional-grade yield remains robust.

Chain dynamics

| Rank | Chain | RWA TVL | 30-day Δ | Share shift |

|---|---|---|---|---|

| 1 | Ethereum | $8.33 B | ▲10.7% | 52.5% share (↑) |

| 2 | zkSync Era | $2.40 B | ▼0.8% | Private-credit lull |

| 3 | Polygon | $1.14 B | ▲2.1% | Stable |

| 7 | BNB Chain | $447 M | ▲22% | Second month of outsized inflow |

| 8 | Avalanche | $355 M | ▲88% | Driven by Republic NOTE & OpenTrade vaults |

| 5 | Stellar | $533 M | ▲12% | Gold tokens and WisdomTree issuances boost TVL |

Signal: while Ethereum tightens its grip, alternative L2s and app-chains demonstrate how single-program launches (Avalanche’s tokenized ETFs, BNB’s treasury wrapper) can materially move market share off a low base.

Commodities & other themes

- PAXG rises 6% MoM to $1.02 B, flipping XAUT for the top gold slot.

- WisdomTree’s WTGOLD mints on Stellar (▲6% MoM) and underlines renewed commodity interest as rate-cut expectations creep into macro discourse.

- Top transfers list is dominated by USTB (Superstate), PAXG, and multiple Solana-based AAPLx blocks, showing both “cash-like” and equity-synthetic assets are actively moving.

Flows & investor behaviour

- Holder growth keeps pace with price expansion → organic adoption, not just whale inflows.

- Issuer count inches up to 274, with Fidelity’s arrival highlighting trad-fi momentum.

- Transfer mix splits between Treasuries, gold, and tokenized blue-chip equities—suggesting balanced portfolios rather than single-theme speculation.

What to watch into late September

- BUIDL vs. FDIT vs. WTGXX: will Fidelity’s launch spark fee compression across treasury wrappers?

- Avalanche follow-through: can Republic’s NOTE and OpenTrade vaults sustain the chain’s 88% MoM TVL leap?

- zkSync reboot: private-credit issuance calendars hint at a mid-month bump—watch Tradable and Goldfinch pools.

- Commodity spread: does silver (SLVon) or oil (JSOY_OIL) follow gold’s lead as inflation hedges?

Bottom line

RWAs just posted another all-green month: value, users, and issuer count each hit all-time highs. Two lanes continue to define the market:

- “Cash-like” Treasuries—still the anchor but increasingly competitive as new issuers arrive.

- “Yield & beta” products—private credit, crypto carry, and equity synthetics now account for the bulk of incremental growth.

With stablecoin liquidity advancing in parallel and large trad-fi names (Fidelity, Deutsche Bank pilot, HKMA licenses) entering the arena, tokenized real-world assets are moving from proof-of-concept to mainstream financial plumbing.

{kind=link}