RWA Weekly — 27 October 2025

RWA value hits $34.9B as gold, credit, and multi-chain growth drive momentum in real estate tokenization news today.

TL;DR

- On-chain RWAs climb to $34.88B (+12.2% MoM)—a fresh all-time high as October draws to a close.

- User base grows: 508,740 holders (+8.6%), 228 issuers, highlighting persistent inflows and new product launches.

- Treasuries remain the core—BlackRock’s BUIDL, Franklin’s BENJI, Ondo’s OUSG, and Circle’s USYC headline inflows, while Superstate’s USTB and WisdomTree’s WTGXX stabilize after turbulent weeks.

- Gold tokens outperform again: XAUT $1.61B (+73%), PAXG $1.37B (+24%), pushing metal-backed on-chain AUM past $3B for the first time.

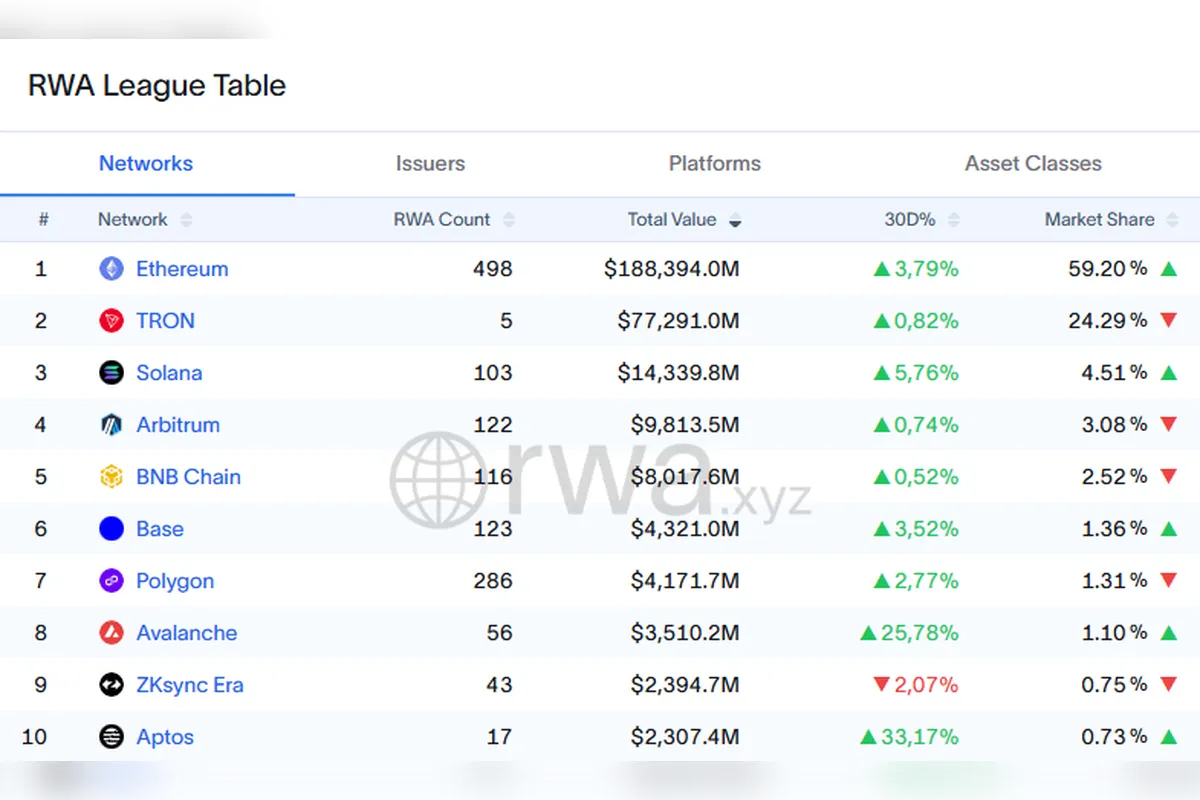

- Major chains rotating: Ethereum’s RWA share tapers (51.7%), while avalanche, Aptos, and Polygon all deliver breakout 30-day jumps; Arbitrum maintains +128% momentum amid credit/ETF launches.

Market Snapshot (As of Oct 27, 2025)

| Metric | Value | 30d Δ |

|---|---|---|

| Total RWA | $34.88B | +12.18% |

| Holders | 508,740 | +8.57% |

| Issuers | 228 | +3 |

| Stablecoin Value | $296.32B | +2.47% |

Context: Settlement liquidity remains robust, and user growth signals sticky adoption—RWA rails are primed for more volume through Q4.

Treasuries: Rotation, Not Retreat

- BUIDL (BlackRock): $2.85B (+33%) still leads the wrapper league.

- BENJI: $852M (+19%)—Franklin Templeton’s pace recovers.

- OUSG: $789M (+8.7%), USYC: $718M (+12.8%), WTGXX: $616M (+10%). Circle’s and WisdomTree’s wrappers keep attracting liquidity.

- USTB (Superstate): $503M (–6.6% monthly)—downshift after a record run.

Rotation theme: Investors aren't leaving treasuries; inflows reflect cost/yield chasing across wrappers and bi-directional recycling after fee shocks.

Private Credit & Carry: Growth Rebounds

- JAAA (Centrifuge AAA CLO): $1.01B (+29%)—largest credit pool.

- USCC (Superstate): $422M (+69%)—carry strategies catch tailwind as stables rotate.

- Midas mF-ONE: $167M (+30%); ULTRA: $136M (flat); niche credit strategies hold.

- ACRED: $128M (+1%)

- Product rotation into flexible, automated strategies keeps liquidity sticky and cross-chain.

Commodities: Gold Surges, Silver Recovers

- XAUT (Tether Gold): $1.61B (+73%)—leads metal-backed tokens.

- PAXG (Paxos Gold): $1.37B (+24%)

- WTGOLD (WisdomTree): $1.93B (+10%). On-chain gold AUM well above $3B.

- SLVon (tokenized silver): $5.05M (+5%)—growth cools after last week's spike.

Insight: Commodities diversify portfolios—gold flows respond to macro and stablecoin yield shifts.

Networks & Structure: Multi-Chain Momentum

| Chain | TVL | 30d Δ | Market Share |

|---|---|---|---|

| Ethereum | $11.33B | +8.3% | 51.7% (downtrend) |

| Polygon | $1.65B | +41% | 7.53% (rising) |

| Avalanche | $1.24B | +68% | 5.67% (rising) |

| Aptos | $1.23B | +70% | 5.60% (rising) |

| Arbitrum | $879M | +128% | 4.01% (stable) |

| Stellar | $638M | +26.6% | 2.91% (rising) |

- Ethereum’s share dips as the multi-chain race heats up; alt-L1s and L2s gain, pulling flows for newly launched RWA products.

- Polygon, Avalanche, Aptos: rapid growth driven by alternative wrappers and regional experimentation.

Flows & Investor Behavior

- Top transfers: thBILL, XAUT, TLTon dominate the tape (~$100K batches)—short-duration wrappers & gold remain hedges of choice.

- User count up 8.6%—retail and institutional participation broadens, even as total TVL grows slightly faster than wallets, signaling larger average tickets.

What to Watch

- Treasury wrapper fee wars: As more wrappers compete on yield and cost, expect higher liquidity migration and innovative fee campaigns in Q4.

- Alt-L1s and L2s: If Polygon/Aptos momentum sustains, could flip market share away from Ethereum further.

- Private credit issuance: JAAA and USCC lead, but pipeline for DeFi tradables could see a Q4 spike.

- Metal-backed tokens: Gold remains the macro hedge with new regional wrappers possible.

Bottom Line

RWAs hit another high above $34B—market is broadening, users are growing, and product innovation continues.

Treasuries anchor risk-off strategies while yield/carry credit pools and gold tokens pull in diversified flows.

Multi-chain integrations accelerate: Ethereum remains king, but Polygon, Avalanche, Aptos, and Arbitrum are taking larger roles.

With steady volume, expanding stablecoin rails, and retail/institutional adoption both rising, RWAs are poised for more upside as November approaches.