Table of Contents

TL;DR

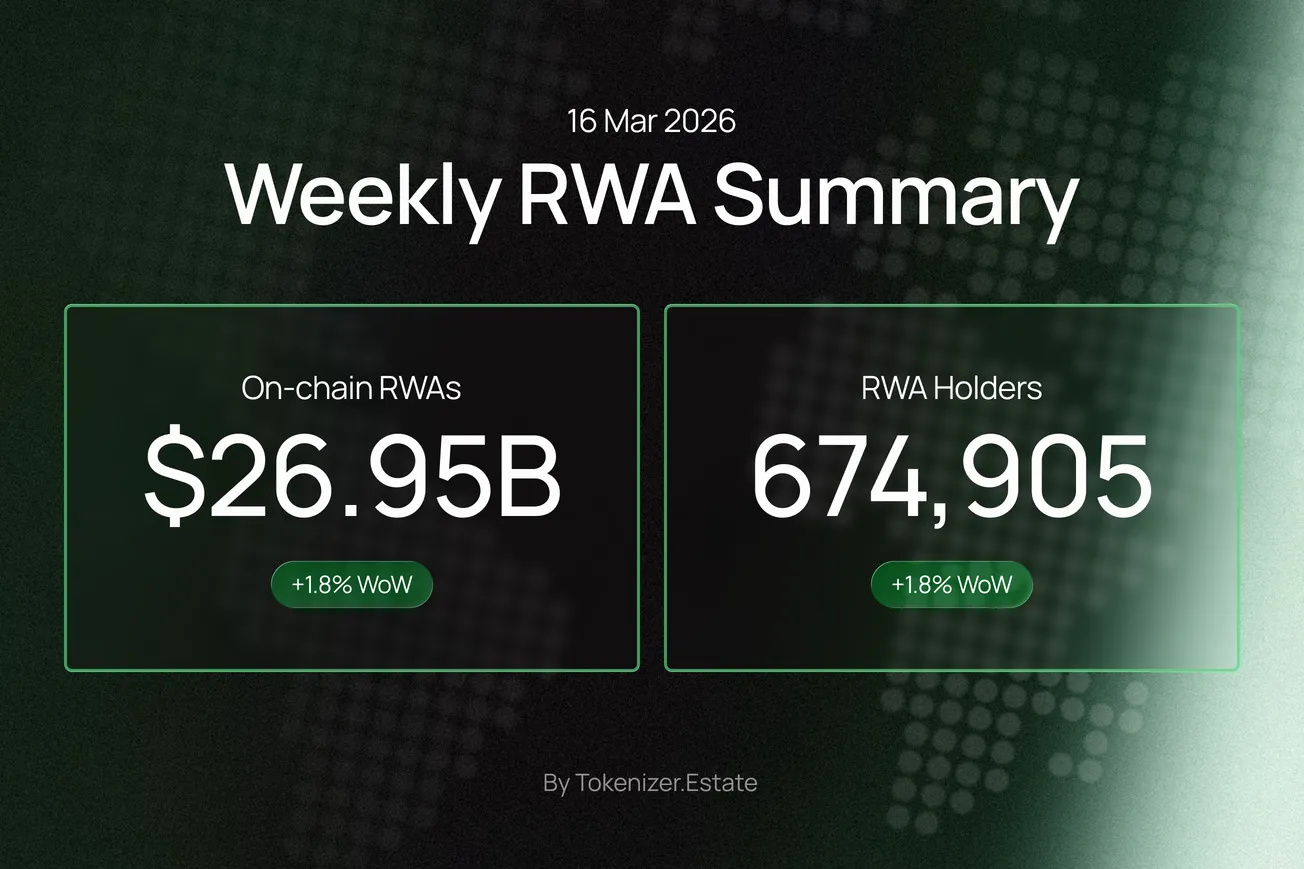

- Aggregate on-chain real-world assets (RWAs) pull back slightly to $28.59 B (▲4.2% MoM).

- Address growth refuses to slow: holders hit 398,673 (▲7.8% MoM), showing retail appetite even as large wrappers reshuffle.

- Sharp rotation inside Treasuries: Circle’s USYC and Ondo’s USDY bleed >$550 M combined, while Superstate’s USTB and Libeara-linked funds absorb the outflow.

- ChinaAMC storms the leaderboard with a $502 M USD money-market token—Asia joins the on-chain T-bill race.

- Credit & carry stay resilient: Centrifuge’s JAAA climbs to $786 M, Superstate’s USCC inches toward $230 M.

- Chain share shifts again: Ethereum TVL slips to 51%, zkSync Era regains momentum, Avalanche cools but BNB Chain presses higher.

- Commodities hold the line: PAXG and XAUT hover near record AUM while tokenized silver (SLVon) and oil (JSOY_OIL) pause.

Market snapshot

| Metric | Value | 30-day Δ | Context |

|---|---|---|---|

| Total RWA on-chain | $28.59 B | ▲4.20% | 2nd-highest ever |

| Holding addresses | 398,673 | ▲7.78% | New peak |

| Active issuers | 205 | ▼6 from last week | Post-summer consolidation |

| Stablecoin float* | $177.56 B | ▼32.8% | Large redemptions in USDC & USDT offset new entrants |

*Stablecoin TVL drop stems from one-off redemptions rather than structural shrinkage; address count still rises.

Treasuries: big shake-out

| Wrapper | TVL | 30-day Δ | Note |

|---|---|---|---|

| BUIDL | $2.10 B | ▼12% | Rotation continues |

| USTB (Superstate) | $296 M | ▲8% | Winner of flows |

| USYC (Circle) | $406 M | ▼22% | Largest weekly outflow |

| BENJI (Franklin) | $501 M | ▼33% | Cash moving to Asia wrappers |

| ChinaAMC CUMIU | $502 M | NEW | Asia’s first $500 M launch |

| ULTRA (Libeara) | $100 M | ▲92% | Yield seekers pile in |

Takeaway: investors are arbitraging fee levels, chain liquidity, and jurisdictional wrappers rather than exiting Treasuries outright—the sector still sits near $6.8 B aggregate.

Yield & credit pulse

- JAAA climbs to $786 M (▲4% MoM) despite risk-off macro chatter.

- USCC (crypto carry) up to $229 M (▲19% MoM).

- Midas mF-ONE vaults past $125 M (▲166% MoM) after integrating real-time NAV disclosure.

Risk-adjusted coupons across top credit pools remain ~9–10%, handily beating on-chain T-bill yields (~4%).

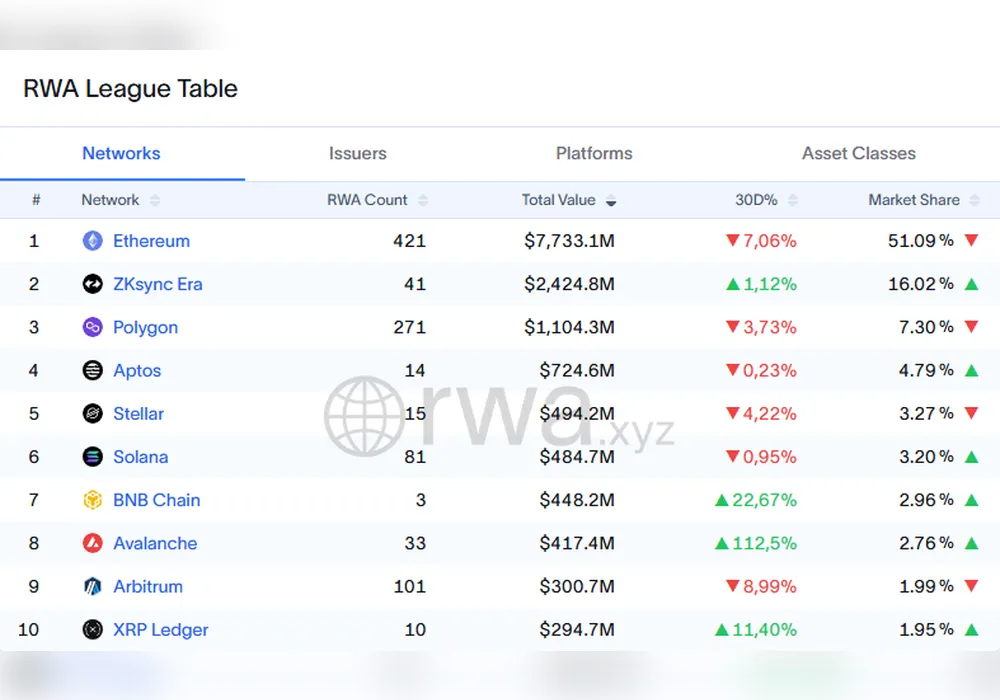

Chain dynamics

| Rank | Chain | TVL | 30-day Δ | Share trend |

|---|---|---|---|---|

| 1 | Ethereum | $7.73 B | ▼7% | Share slips to 51% |

| 2 | zkSync Era | $2.42 B | ▲1% | Credit inflows resume |

| 3 | Polygon | $1.10 B | ▼4% | Soft across wrappers |

| 7 | BNB Chain | $448 M | ▲23% | Treasury products lift TVL |

| 8 | Avalanche | $417 M | ▲113% MoM (but ▼8% WoW) | ETF hype cools |

| 9 | Arbitrum | $301 M | ▼9% | Fewer private-credit closes |

Pattern: value migrates to chains offering native fiat ramps (BNB) or cheap L2 settlement (zkSync), while ETF-driven bursts (Avalanche) prove volatile.

Commodities & other thematics

- PAXG steadies above $1.05 B; on-chain gold market now >$2 B with XAUT and WTGOLD combined.

- Tokenized silver (SLVon) and oil (JSOY_OIL) stall after multi-week rallies, mirroring softer spot prices.

- Top transfers list dominated by USTB packets and PAXG blocks, confirming a “cash-plus-gold” hedging bias.

- UnitedHealth equity token UNHon cracks the top-10 transfer board, underscoring growing demand for tokenized blue chips.

Flows & behaviour insights

- Retail broadening: holder count growth outpaces TVL—smaller tickets are driving activity.

- Issuer pruning: 205 active issuers (down from 274 peak) suggests dashboards are finally de-listing dormant shells.

- Asia factor: ChinaAMC’s $500 M debut shows Asian asset managers can mobilize deposits quickly when local wrappers meet on-chain rails.

What to watch into Q4

- Fee wars in Treasuries: Will BUIDL cut fees to halt outflows?

- zkSync credit calendar: Goldfinch’s $200 M loan closings could extend the chain’s rebound.

- Stablecoin rail rebuild: Stablecoin TVL plunge may reverse as MetaMask’s mUSD and Tether’s USA₮ scale.

- Regulatory catalysts: EU finance ministers’ digital-euro roadmap and Thailand’s green-asset token rules could seed new RWA verticals.

Bottom line

The headline RWA market cap dipped from last week’s peak, but beneath the surface capital is re-allocating, not exiting. Asia-based wrappers, cheaper fee structures, and multi-chain liquidity are reshaping the landscape faster than legacy incumbents can react. With nearly 400 K addresses now holding tokenized real-world assets and credit yields holding firm, the secular adoption story remains intact—setting the stage for a fresh push toward the $30 B milestone once the current rotation stabilises.

{kind=link}