Table of Contents

TL;DR

- On-chain RWAs reached $33.71B, down 2.25% over 30 days, indicating a mild consolidation after sustained growth.

- Holder count rose strongly to 538,863 (+10.4%), confirming broadening participation despite TVL cooling.

- Active issuers steady at 249, sustaining a reliable supply pipeline.

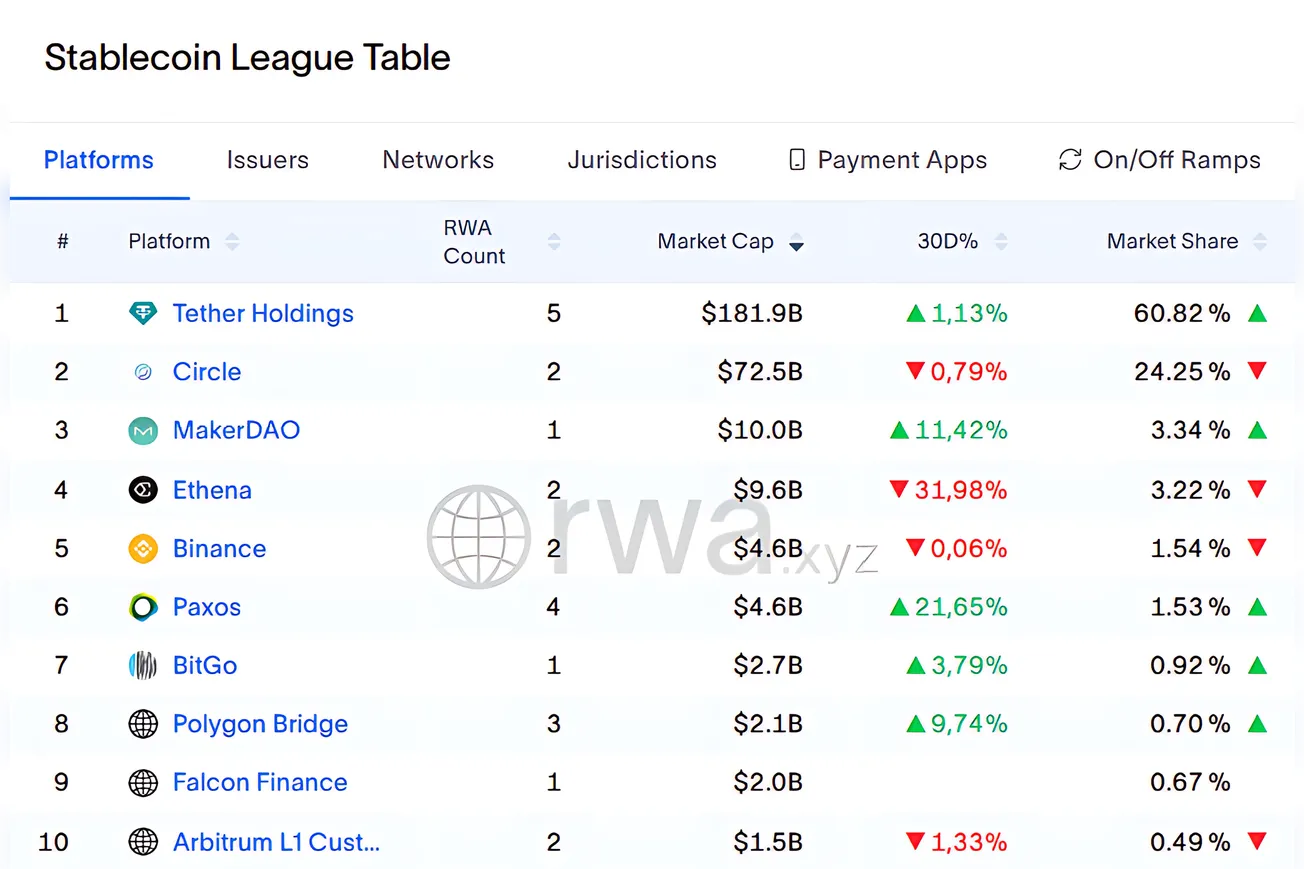

- Stablecoins remain a robust liquidity backbone at $299.0B (+0.42%), supporting settlement and transfers with 202.73M holders (+3.15%).

- Treasury wrappers rotate capital: Circle’s USYC leads with +51% growth to $1.08B, while BlackRock’s BUIDL and Superstate’s USTB saw modest declines.

- Private credit gains traction - Maple’s syrupUSDT and syrupUSDC rise +79% and +51%, centring above $1.9B combined; Centrifuge’s JAAA inches up +4.5%, sustaining ~10% APR yields.

- Commodities steady, anchored by gold tokens (XAUT, PAXG, GLDx), with Solana-based GLDx transfers leading weekly volumes.

- Chain activity diversifies: Ethereum holds $11.8B (-9.2%), while Polygon (+43%), Avalanche (+67%), Aptos (+68%), BNB Chain (+57%), and Solana (+15%) gain market share on new wrappers and alt-L1 launches.

Market Snapshot (as of Nov 17, 2025)

| Metric | Value | 30-day Δ | Signal |

|---|---|---|---|

| Total on-chain RWAs | $33.71B | ▼ 2.25% | Sideways consolidation |

| Holding addresses | 538,863 | ▲ 10.4% | Wider participation |

| Active issuers | 249 | — | Steady supply pipeline |

| Stablecoin backdrop | $299.0B | ▲ 0.42% | Deep liquidity runway |

Stablecoins continue to outpace RWA growth in nominal inflows, keeping on-chain settlement rails liquid. The RWA-to-stablecoin ratio now sits around 1 : 9, highlighting room for further asset migration.

Tokenized Treasuries: Broad Rotation

Tokenized U.S. Treasury exposure remains the largest on-chain category, but the internal allocation continues to churn.

Leaders:

- Circle’s USYC: surged +51% this month to $1.08 B TVL, now the fastest-growing Treasury wrapper.

- WisdomTree’s WTGXX: +17%, approaching $695 M, signaling sustained institutional inflows.

- Theo’s thBILL : +19%, maintaining momentum among smaller wrappers.

Soft spots:

- BlackRock’s BUIDL: down 11.4% to $2.52 B, though still #1 by size.

- Superstate’s USTB: -5.9%, rotation toward Circle and WisdomTree wrappers evident.

Takeaway: Flows show optimization across custodians and networks rather than capital flight. Investors rotate between wrappers in search of better yields, liquidity routing, and transparency tools.

Private Credit: Quiet but Steady

Private credit remains the gravitational center of yield.

- Maple’s syrupUSDT & syrupUSDC posted MoM gains of +79% and +51%, respectively, pushing combined TVL above $1.9 B.

- Centrifuge’s JAAA inched up 4.5% to $1.01 B — still the flagship institutional vehicle.

- Average on-chain APRs in active credit pools ≈ 10–11%, holding stable against Treasury yields.

Interpretation: Slower expansion reflects credit maturity and repayments rather than risk aversion; the segment continues to absorb liquidity from investors seeking steady, higher income.

Chain Dynamics

| Rank | Network | RWA TVL | 30D Δ | Coverage |

|---|---|---|---|---|

| 1 | Canton | $372.7B* | ▼3.78% | Institutional-only (minimal on-chain activity) |

| 3 | Ethereum | $11.8B | ▼9.24% | Still ~98% of public-chain RWAs |

| 5 | Polygon | $1.6B | ▲43.3% | Fastest-growing public chain |

| 6 | Avalanche | $1.2B | ▲67.2% | Institutional credit issuances driving surge |

| 7 | Aptos | $1.2B | ▲68.5% | Signals push toward Move-based RWA infra |

| 8 | BNB Chain | $953M | ▲57.1% | Expanding with stablecoin diversification |

| 9 | Solana | $796M | ▲15% | Tokenized equities (xStocks) fueling growth |

Interpretation: Ethereum still anchors issuance but RWA growth is dispersing across multi-chain ecosystems — especially Avalanche, Polygon, and Solana, where tokenized stock wrappers are gaining traction.

Sector Highlights

- U.S. Treasuries remain dominant, accounting for ~45% of total RWA market cap.

- Private Credit holds ~30%, driven by institutional money-market vaults.

- Commodities, mainly gold tokens (XAUT, PAXG), rallied ~2% after a soft October.

- Tokenized Stocks on Solana and Ondo continue to expand, signaling investor appetite for fractional equity exposure.

What to Watch Ahead

- Rebound in Ethereum Treasuries: Will BUIDL regain inflows post-month-end rotations?

- Alt-chain scaling: Avalanche and Polygon could challenge Ethereum’s RWA share if double-digit growth sustains into December.

- Institutional signals: More regulated wrappers (Fidelity, Franklin) may compress yield spreads between legacy and DeFi-native RWA.

- Commodities rotation: Gold stable, but oil and ESG-linked instruments could attract next inflow wave.

Bottom Line

Even after a modest pullback in TVL, the RWA landscape remains healthy and diverse. With participation surging, credit yields stable, and cross-chain integration accelerating, the sector is maturing into crypto’s most resilient growth story. Expect another re-acceleration in December as capital redeploys post-rotation and new issuers join across Avalanche, Aptos, and BNB Chain.

{kind=link}