Table of Contents

TL;DR

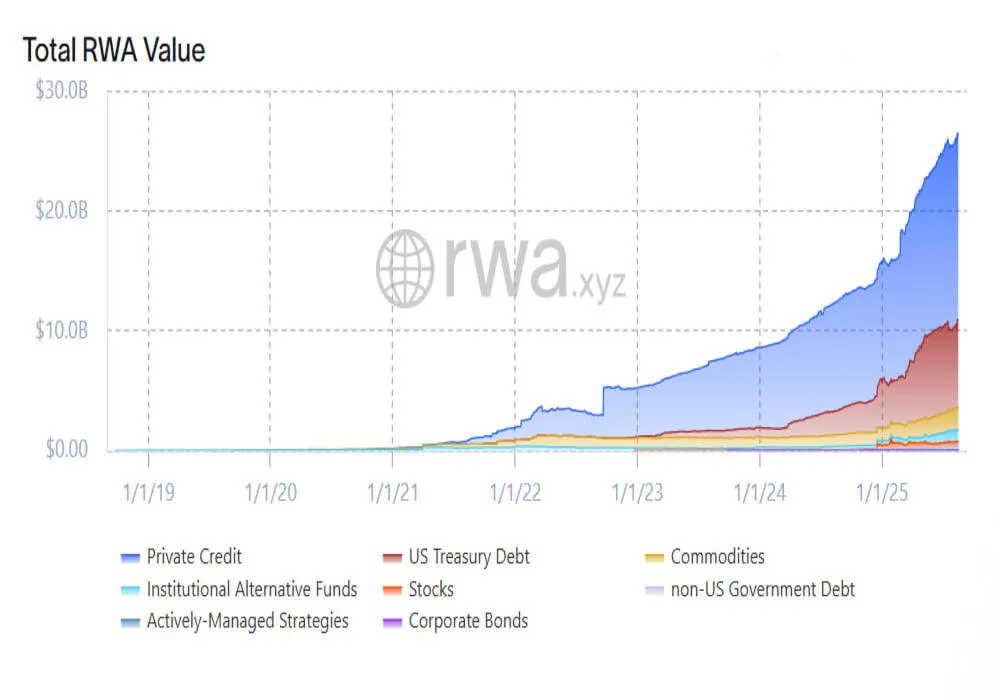

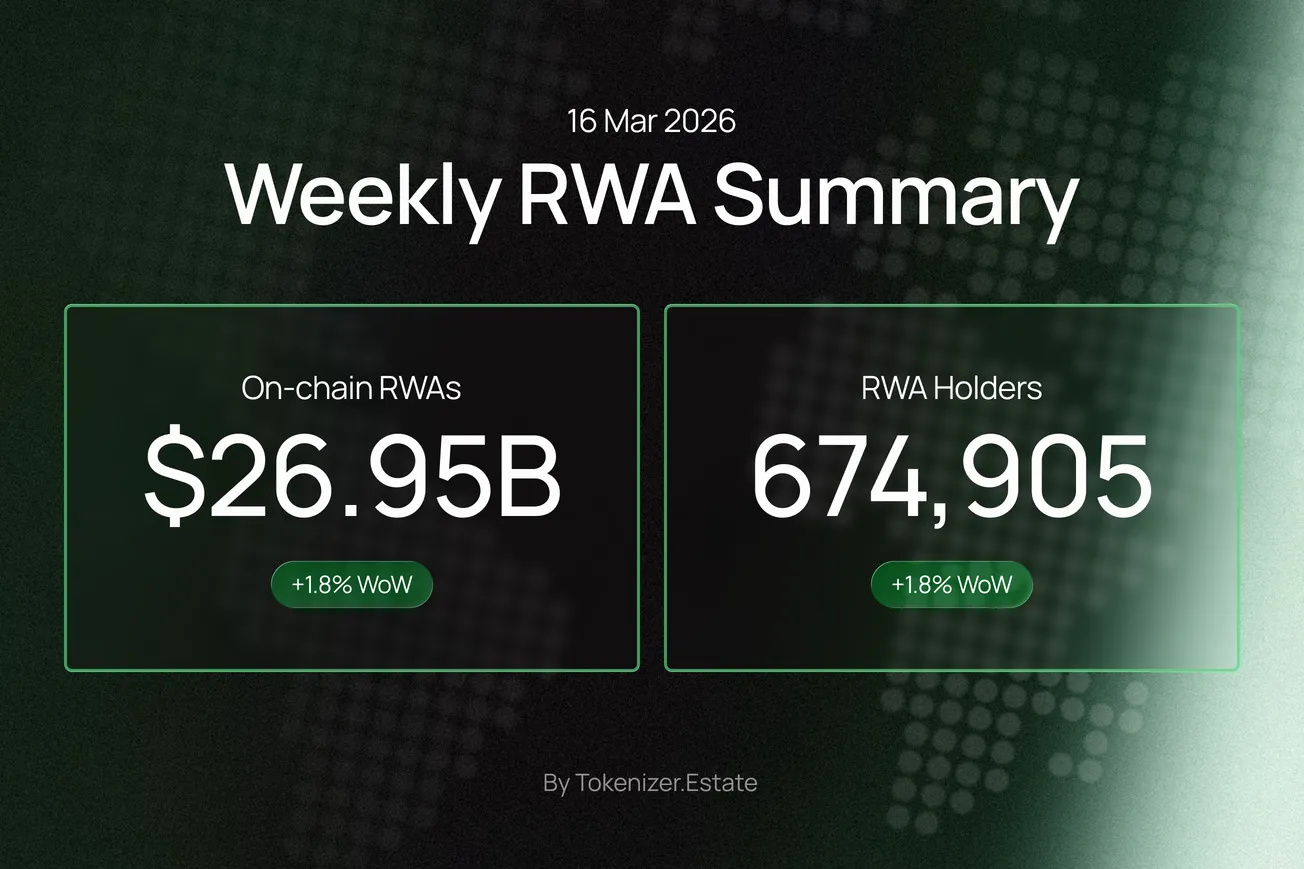

- On-chain RWAs sit around $26.6B, up ~2.6% over 30 days. Holder counts are rising double-digits.

- Tokenized Treasuries total about $6.7B; leadership is split across Securitize (BUIDL), Ondo, Franklin Templeton, and WisdomTree, with notable 30-day divergences.

- Private credit is the hot lane: $15.5B in active loans, $28.6B total originated, average APR near 9.8%.

- Networks: Ethereum still leads by value, but zkSync is gaining share; Plume shows the fastest 30-day growth among the top ten.

Market snapshot (as of Aug 15, 2025)

- Total RWA on-chain: $26.59B, +2.64% vs. 30 days ago.

- Holders: 355,085, +12.71% vs. 30 days ago.

- Stablecoins (context): $264.30B market value, 188.90M holders.

These headline numbers set the tone: the base is firm and the user base keeps broadening.

Treasuries: steady base, mixed flows

Tokenized U.S. Treasuries sit at $6.72B (7-day move: –1.59%). Market share by protocol shows Securitize in front ($2.37B, 35% share), Ondo next ($1.39B, 21%), then Franklin Templeton Benji ($694M, 10%) and WisdomTree ($600M, 9%). The dispersion in 30-day moves is striking: WisdomTree is up strongly, while Superstate shows notable drawdown—signs of rotation within “cash-like” products rather than a retreat from the category.

Single-asset check: BlackRock’s BUIDL fund remains one of the largest line items (~$2.42B market cap), though down on a 30-day basis—again pointing to reallocations across treasury wrappers and venues rather than demand vanishing.

Private credit: where the action is

RWA.xyz tracks $15.52B in active private-credit loans and $28.63B total originated, with a current average APR ~9.76% across 2,571 loans. For yield seekers, this is the center of gravity right now.

Platform spotlight — Tradable (zkSync): about $2.06B in tokenized assets (+2.77% in 30 days), concentrated on zkSync Era. Deal inventory spans BNPL, legal-fee receivables, fintech working capital, and more—with ticket sizes from ~$20M to ~$268M per pool. This looks like institutional private credit, packaged into programmatic notes and term loans.

Networks & market structure

Ethereum still carries the largest share of RWA value ($7.07B, 55% market share). The runner-up story, however, is zkSync Era ($2.44B, 19% share) with positive 30-day momentum—mirroring the private-credit concentration noted above. Plume enters the top-10 by value with the fastest 30-day growth rate among peers, showing that specialized L2s/appchains can quickly matter once a flagship program lands.

Investors & flows

Two things can be true at once:

- Holders are growing fast (double-digit 30-day growth), indicating more addresses are touching RWAs.

- Assets are rotating between wrappers and venues (e.g., BUIDL’s 30-day dip alongside gains for others in treasuries).

Net, this looks like deeper engagement rather than hot-money churn.

What to watch next

- Treasury rotation: Will WisdomTree’s momentum persist, and does Superstate’s drawdown stabilize? These give clues on investor preferences for wrappers, fees, and integrations.

- zkSync’s private-credit flywheel: If Tradable and peers keep listing sizeable pools, zkSync’s market share could climb further.

- Issuer concentration: Securitize continues to anchor the treasuries stack—keep an eye on whether newcomers narrow the gap or if incumbents deepen liquidity first.

- Stablecoin backdrop: With stablecoin value north of $260B, RWAs benefit from deep, dollar-like liquidity rails—useful for subscriptions/redemptions and settlement.

RWAs show steady, modest growth with a clear shift in mix: treasuries remain the anchor while private credit drives most of the incremental expansion. Flows are rotating across wrappers and venues rather than exiting the category. Ethereum continues to hold the center of gravity, and certain L2s—especially zk-focused rails—are gaining share on the back of private-credit programs. Participation is broadening and liquidity is consolidating around a handful of large issuers and platforms. Net effect: the market looks more mature, multi-chain, and segmented between “cash-like” assets and higher-yield credit, supported by increasingly professional infrastructure.

{kind=link}